Outlook

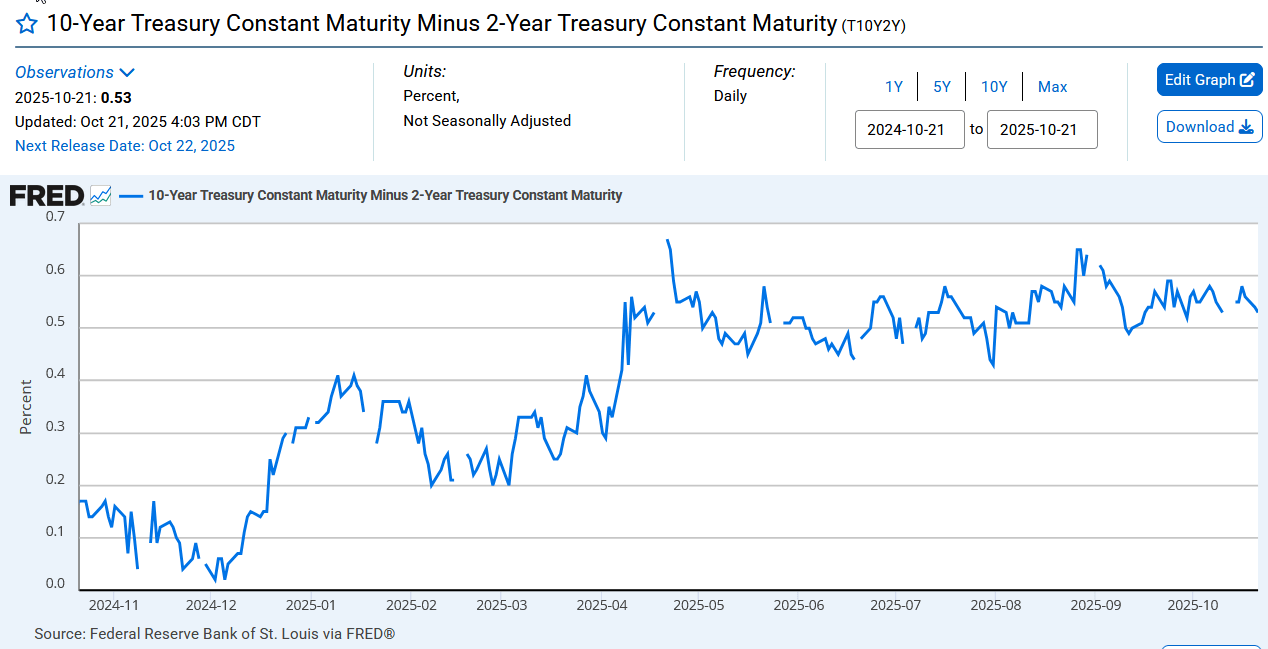

We await the US Sept CPI on Friday. Before then, the Treasury will auction a 20-year today. The 20-year yield has been falling since June—where are the bond vigilantes?—and the 2/10 spread has gyrating around 0.4-0.65% since May, after the leap on the start of the tariff war in April. See the chart from the St. Louis Fed.

This is screwed up. The correlation of currencies with their yields is not consistent but it’s fairly high most of the time. And the yield is highly correlated with expected inflation, since the premium is protection against inflation eroding real return. This is classic stuff and when it gets topsy-turvy, traders in both markets get confused and take puzzling positions.

Realistically, everyone knows the Fed is wrong by projecting only a one-time, transitory jump in inflation from tariffs. The Fed will get a partial comeuppance on Friday when CPI comes in over 3% and is the 5th straight month of rises. As Reuters notes, “That would put both headline and ‘core’ inflation more than 1 percentage point above the Fed’s 2% target, raising the question of whether it’s still a target at all.”

In a special Reuters report on inflation: “Fernando Martin at the St. Louis Fed, wrote last week that an updated analysis of national inflation trends suggests the United States may now be in a ‘persistent above-target regime.’” This seems obvious to us mere mortals but heavy-duty statistics do make the point.

The analysis is wide but what stands out is this: “The purchasing power of $1,000 today would be reduced to $820 in 10 years time under a steady 2% annual inflation scenario. It falls to $744 in a 3% regime. Can the U.S. ‘eat’ that without households demanding higher wages or businesses seeing purchases slump? Maybe, but no one’s 100% sure.

What’s more notable, however, is that almost no one seems to care right at this juncture.”

Forecast: The stock market is confused. Can AI keep going or is it time for a retreat? It’s not clear that earnings from the likes of Netflix (or banks) should affect the whole market, but again, when you have a giant momentum trade, a flash crash is always a possibility.

Then there’s the yield story, where expected inflation is NOT being priced in. You can make the case that gold and other metals are actually a side-show of the FX market and gold took a nose-dive because the dollar was resuscitated. Those resuscitation instances have tended to be short-lived, but never mind. The 10% dollar drop on Trump remains so little retreats are nothing to write home about, let alone let off a flash crash.

The Big Picture is a weak dollar for all the reasons already well-known, with inflation getting added more firmly to the list on Friday. That includes a recovery in gold. But there is no comfort here. On the weekly euro chart, the ATR breakout number is 1.1001 and the 200-week moving average is 2.-0838. Not out of the question. Therefore, do not be in hurry to assume a short-lived dollar rebound this time. It goes without saying we don’t’ like it. It’s not logical. But currency trading is often not logical.

Tidbit: Folks couldn’t stop talking about the gold bubble and when it might burst. To figure that out, consider the reasons gold has risen over 50% in the first place. Which of those many reasons might get fixed and go away?

So, what happened yesterday? The most important thing about gold is that it had become a momentum trade, no fundamentals needed. So the reason gold fell is the cascade that followed some big sale and set off Herd Instinct. This is exactly like the group retreat when the herd leader spots a lion ahead and turns away. A flash crash like this is often without a specific cause, just a big seller or two that ignites fear.

These days it goes without saying that the first sellers could be real profit-taking, position-paring humans. The next sellers could be AI systems calibrated to sell as certain numbers come up. As noted over 20 years ago, what was called “algo trading” then is suspected of causing more than one stock market flash crash.

Various reports make up reasons, but nobody really knows why those first sellers got the willies. The “reason” depends on which report you are reading. The WSJ says expectations of a US-China trade deal. A Kitco Metals analyst cited “Better risk appetite in the general marketplace early this week is bearish for the safe-haven metals.” Citi says an end to the shutdown and US-China trade deal.

We could get an end to the government shutdown in the coming weeks. When the US government ends the shut-down, it’s not necessarily a negative for gold. We are still stuck with a humungous deficit.

As for the China trade deal, don’t count your chickens. We could get another pause before the Nov 1 deadline that might look like an end might be near. Analysts say this is a false hope and the end is nowhere near, but that won’t stop a sense of relief and therefore a pullback in gold.

It’s obvious to a vast majority of analysts that China has been winning long before Trump came along and has continued to excel and beat out the west on many, many fronts, including owning a third of the top 100 ports, sustaining exports, making far more advances in clean energy, robotics and high tech, and more. It’s equally obvious that Trump is going to TACO.

Another reason for gold to come back is tariff-driven slower growth/recession. But even the World Bank/IMF admit tariffs have not done much damage so far.

Another pro-gold factor is the likelihood that the Fed gets taken over by the White House. Trust in the Fed vanishes instantly and gold benefits. As for any reprieve in the over-indebtedness, forget about it. Tariff revenues are not nearly enough. Estimates have it that tariff revenues so far are about $200 billion and the deficit for 2025 will be $1.78 trillion.

Then there’s geopolitical risk, including Palestine and Ukraine, and no matter what any politician says, including Trump, peace is not in sight. We also have ongoing central bank diversification away from Dollars, much of it going to Gold.

Add the risk of inflation finally rising, whether tariff-driven or other causes, including rising wages because of the labor shortage. Most economists firmly believe inflation cannot fall to the Fed’s supposed 2% target under a tariff regime, even if the US imports/GDP is pretty small (about 14%). It just hasn’t happened yet. Exporters and US importers are eating the tariffs so far. That will end. See the next Tidbit, too.

Should the stock market falter—on disappointing earnings or for any other reason—gold goes in the opposite direction. Yield no longer matters, only safety.

And the Big Factor: Trump and his lack of facts, reasonableness, and his ignorance of economics and history, let alone decent manners. This is the guy who posted a photo of himself in a crown piloting an airplane dumping excrement on the No King protesters. He presumably thought it was funny but imagine how it was viewed in Beijing or Tokyo. Trump, not tariffs, is the top factor devaluing the dollar. Krugman, among others, says he is out of touch with reality. It could be so.

The Big Banks keep modifying their forecasts as each new price overwhelms the old forecasts. Something around $5000 is where they mostly stand today. There are more reasons to expect ongoing gains than to expect a sustained pullback. Yes, we have a pullback, but there are no reasons for it to convert into a reversal. Next up will be a slew of charts showing where it might end and return to the rally. Pullbacks are, alas, common, and often just as confusing as this one.

We imagine Kitco got it right—a switch in appetite for more risk. If so, then the dollar gain at the same time as the gold retreat means the dollar is a risk asset now. Well, yes, it is. It’s not Nigeria but look at all those negatives! This is a little iffy because the 10-year yield is still down and lower, implying a flight-to-safety mood. When the yield is down but the dollar is up, everyone is confused.

What happened to safe haven? A currency can’t be both, can it? Well, why not? A risky thing when risk is in favor and a risk-protection when the market is feeling risk-off. Actually, we did see the euro exhibit some of this dual personality during the Grexit crisis, although it wasn’t named risk-on and risk-off then.

Tidbit: Yahoo!Finance reports Goldman estimated in an Oct 12 report “Americans are set to pay more than half of President Donald Trump’s tariff costs as companies raise prices… US consumers will likely shoulder 55% of tariff costs by the end of the year, with American companies taking on 22%… Foreign exporters would absorb 18% of tariff costs by cutting prices for goods, while 5% would be evaded.”

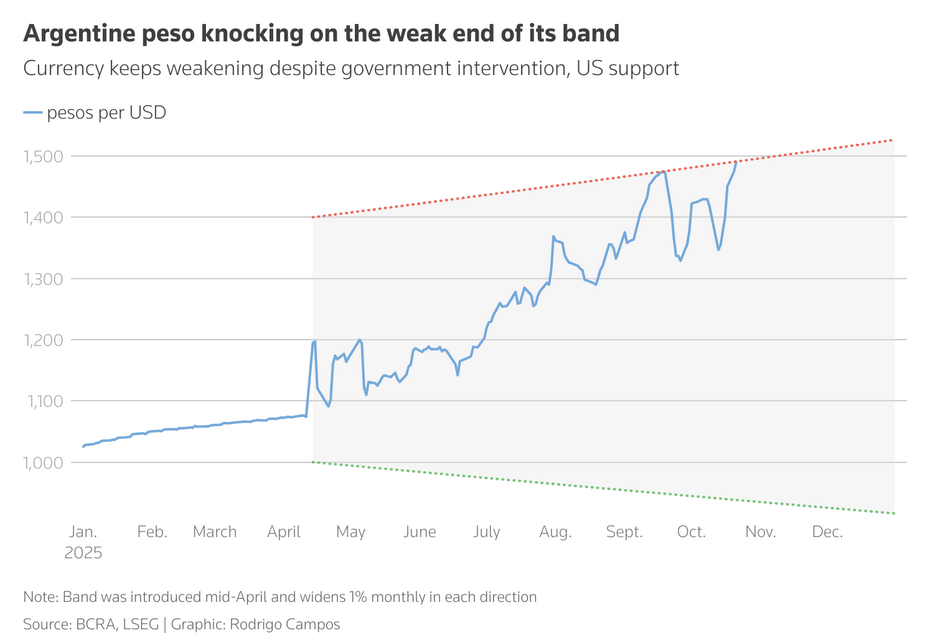

Tidbit: The US “rescue” of Argentina is not working. Reuters reports “Argentina’s central bank sold $45.5 million from its reserves on Tuesday to support the exchange rate, after the peso reached the upper limit of the central bank’s floating band despite U.S. support and a $20 billion currency swap to guarantee payment of the next public debt maturity. The intervention came as uncertainty in the market ahead of Sunday’s legislative elections spurred a shift toward dollar assets.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!