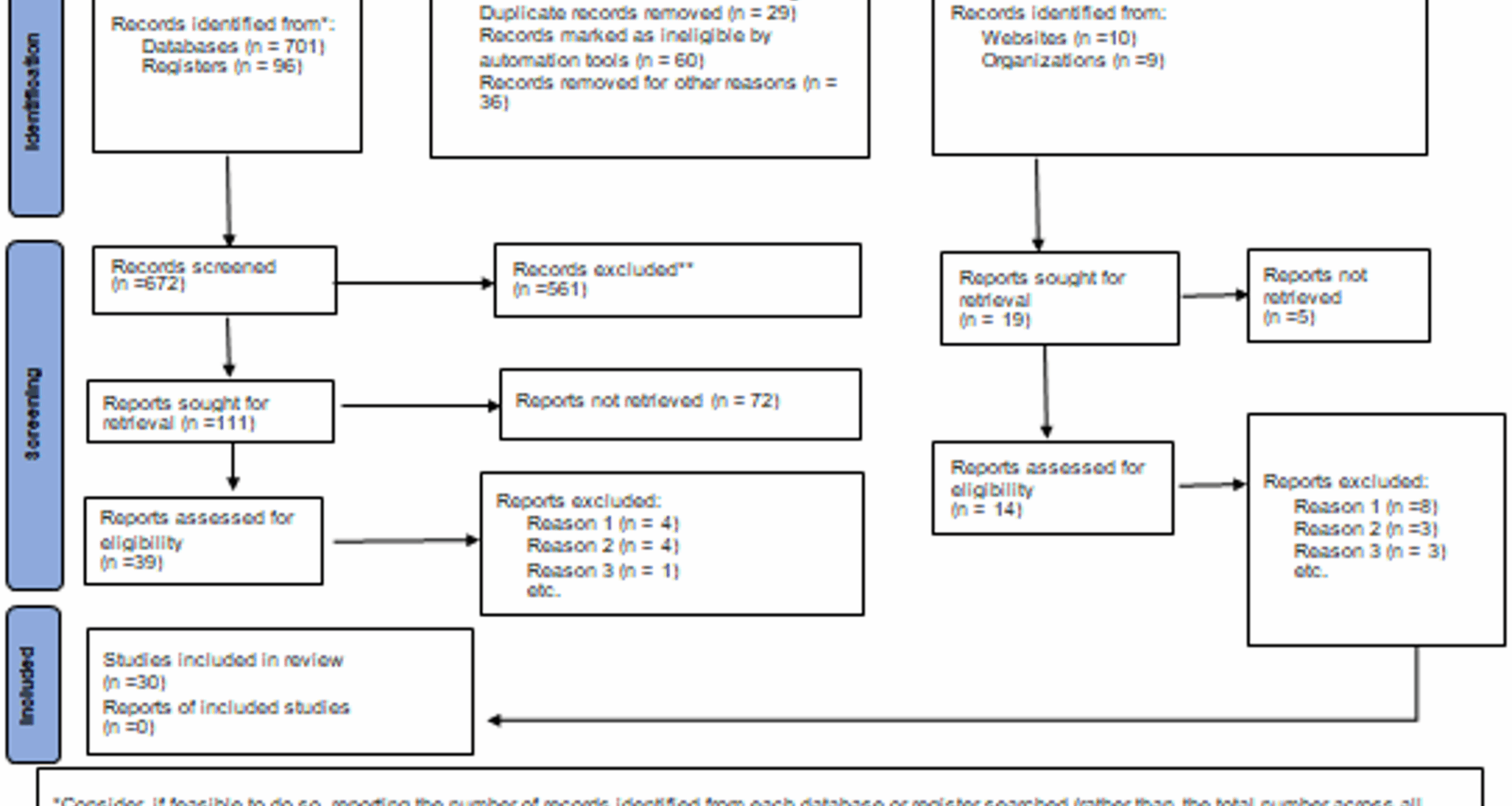

Most studies were conducted in high-income countries (USA) and most studies were cross-sectional (80%) and had medium-samples (50%). The selected studies were conducted from 1996 to 2024.

The review revealed significant regional variations in the focus and findings of financial resilience research, shaped by differing economic conditions, institutional frameworks, and sociocultural contexts.

High-Income countries

The majority of studies on financial resilience were conducted in high-income countries (HICs), such as the United States, Australia, and Western European nations. Research in these regions predominantly examined financial fragility—defined as the inability to cope with unexpected expenses—and the role of financial literacy in mitigating economic vulnerability. A recurring theme was the impact of the COVID-19 pandemic, which exposed financial precarity even in affluent societies. For instance, Clark et al. (2022) found that households with strong financial planning skills and effective debt management strategies were better equipped to navigate pandemic-induced economic disruptions. Their study highlighted that access to emergency savings, diversified income sources, and financial education played a crucial role in sustaining resilience during crises. Additionally, research in HICs often explored the effectiveness of government interventions, such as stimulus packages and unemployment benefits, in buffering financial shocks. However, some studies pointed out gaps in policy coverage, particularly for gig workers and low-income households, suggesting that systemic inequalities persist even in wealthy nations.

Low- and Middle-Income countries (LMICs)

In contrast, studies from LMICs including India, Kenya, and Rwanda focused more on informal coping mechanisms due to limited access to formal financial safety nets. Households in these regions frequently relied on strategies such as borrowing from informal lenders, selling assets, or depending on community support networks to manage financial shocks. Nkurunziza et al. (2023), for example, investigated shock-coping mechanisms in rural Rwanda and found that household characteristics (e.g., size, education level, and asset ownership) significantly influenced resilience. Their study also emphasized that the nature of the shock (sudden vs. recurring) shaped coping behaviors for instance, droughts or health emergencies forced families to liquidate assets, while income fluctuations led to increased reliance on social networks. Another key finding from LMIC research was the role of microfinance and community-based savings groups (e.g., ROSCAs) in enhancing financial resilience. However, some studies cautioned that excessive reliance on informal borrowing could lead to debt traps, particularly when interest rates were high.

Components of financial resilience

Financial resilience is a multidimensional construct shaped by a combination of economic, behavioral, social, and institutional factors. Understanding these components is essential for developing interventions that strengthen individuals’ and households’ ability to withstand financial shocks.

Economic resources

The foundation of financial resilience lies in economic resources, including stable income, savings, and manageable debt levels. Research consistently shows that individuals with higher and more predictable incomes are better positioned to absorb financial shocks, such as job loss or medical emergencies. Savings act as a critical buffer, allowing households to cover unexpected expenses without resorting to high-interest loans or asset depletion. However, disparities exist—low-income households often struggle to build savings due to living paycheck-to-paycheck, making them more vulnerable to economic disruptions. Effective debt management is another crucial aspect, as excessive debt (particularly high-interest or predatory loans) can erode financial resilience over time.

Financial knowledge and behavior

Financial literacy, which encompasses essential skills such as budgeting, saving, investing, and debt management, plays a pivotal role in fostering financial resilience. Research shows that individuals with strong financial literacy are more likely to create and adhere to budgets, build emergency funds, make informed borrowing decisions, and plan for long-term financial security. Behavioral factors, including self-control and future-oriented financial planning, further strengthen resilience. However, financial education alone is not enough; access to supportive financial systems and products is equally critical to ensure individuals can effectively apply their knowledge.

Social capital, defined as networks of trust, reciprocity, and institutional support, serves as an informal safety net during financial distress. Key forms of social capital include community savings groups, such as ROSCAs and chit funds, which provide interest-free liquidity in emergencies. Informal insurance networks, such as family or clan support, enable reciprocal assistance during crises, while digital social capital including crowdfunding and peer-to-peer lending offers rapid financial support through online platforms. Additionally, policy-led social capital, such as government welfare programs, provides public safety nets like unemployment benefits or food subsidies. Strong social ties reduce reliance on predatory lenders and help prevent distress sales of productive assets, further enhancing financial resilience.

Access to financial resources, including banking, credit, insurance, and digital payment systems, is another critical component of financial resilience. Financial inclusion ensures individuals have formal mechanisms to manage economic shocks. For instance, credit access can help smooth consumption during income disruptions, though unregulated borrowing may lead to over-indebtedness. Insurance products, such as health, crop, or property coverage, mitigate catastrophic financial losses but remain underutilized among low-income populations due to affordability and trust barriers. Meanwhile, digital financial services, including mobile money and fintech loans, improve accessibility but require robust consumer protection safeguards to prevent exploitation. Together, these elements—financial literacy, social capital, and access to financial resources—form a comprehensive framework for building resilience against financial shocks.

Strategies for enhancing financial resilience

Households employ a mix of proactive and reactive strategies to strengthen financial resilience, with approaches varying based on economic context. One key strategy is income stability and diversification, as relying on a single income source increases vulnerability. Households often engage in multiple income streams, such as combining wage labor with off-farm activities like side businesses or gig work. Investing in skills training also enhances earning potential, reducing financial fragility and alleviating stress-related illnesses linked to income volatility.

Another critical approach is savings and asset management. Building liquid savings whether in cash or mobile money ensures quick access to funds during emergencies. Investing in productive assets, such as livestock or tools, provides long-term security, though it carries the risk of distress sales if immediate liquidity is needed. These strategies contribute to faster shock recovery and help maintain access to essential services like healthcare.

Borrowing and financial assistance also play a role, though with trade-offs. Formal credit options, such as bank loans or microfinance, offer structured repayment plans but may exclude the poorest households. Informal loans from family or moneylenders provide flexibility but often come with high interest rates or social pressure. While borrowing can offer short-term relief, it may lead to long-term debt traps, potentially delaying essential expenditures like healthcare.

In times of financial strain, households often resort to reducing expenditures, cutting back on non-essentials such as leisure, education, or even nutritious food. While this provides immediate cost relief, it can have harmful long-term consequences, including child malnutrition, school dropouts, and overall human capital erosion.

Social networks serve as another vital resilience mechanism. Community support whether through loans, in-kind aid, or emotional backing helps preserve assets and mental well-being. Strong social ties reduce the need for distress asset sales and contribute to improved psychological health.

Finally, insurance and risk transfer mechanisms, such as health or crop insurance, can prevent catastrophic financial losses. However, low trust and affordability issues often hinder widespread adoption. When accessible, insurance mitigates large financial shocks and encourages preventive care utilization.

Policy and research implications

To enhance financial resilience, policies must be tailored to different economic contexts. In high-income countries (HICs), expanding financial education and regulating predatory lending can help households make informed decisions. In low- and middle-income countries (LMICs), strengthening social protection systems and promoting affordable insurance are crucial. Cross-cutting solutions should address behavioral barriers such as present bias through interventions like automatic savings nudges, ensuring households are better prepared for financial shocks. By combining these strategies, individuals and communities can build stronger, more sustainable financial resilience.

This framework highlights that financial resilience is not just about individual actions but also systemic support structures that enable equitable access to resources. Future research should explore intersectional vulnerabilities (e.g., gender, disability) and the role of technology in scaling resilience strategies.

Outcomes of financial resilience

Reduced financial fragility

Financial resilience strategies help reduce financial fragility, enabling individuals and households to better manage unexpected expenses and income shocks. This is often measured by the ability to cover a $2,000 emergency expense within a month.

Improved life satisfaction

Financial resilience is positively correlated with overall life satisfaction. Individuals who are financially resilient report higher levels of well-being and lower financial stress.

Enhanced financial stability

By adopting financial resilience strategies, individuals and households can achieve greater financial stability, reducing their vulnerability to economic shocks and improving their long-term financial health.