The popular narrative on the war with Iran basically sees two options for how things play out: (i) military escalation that could even see “boots on the ground” to reopen the Strait of Hormuz; or (ii) President Trump declaring “mission accomplished” even as the mullahs remain in charge. The problem with the latter scenario is that Iran may keep blowing up oil tankers and infrastructure in an effort to keep oil prices elevated. That would damage the President’s standing into the midterm elections later this year. The problem with the former scenario is that it could result in terrible loss of life on both sides, which could be a debacle for the Republicans in November. Neither scenario is politically viable.

Fortunately, there’s a third option, which in to embargo Iranian oil. The US would announce that any fully-laden tankers leaving Iran’s ports would be intercepted and confiscated, by force if necessary. I highly doubt that anyone would be willing to test US resolve. After all, Iran has been able to close the Strait of Hormuz with a couple of drones and rockets. The pushback to this option – instead – is that it would make the oil shock even worse by taking Iran’s two million barrels a day off the market.

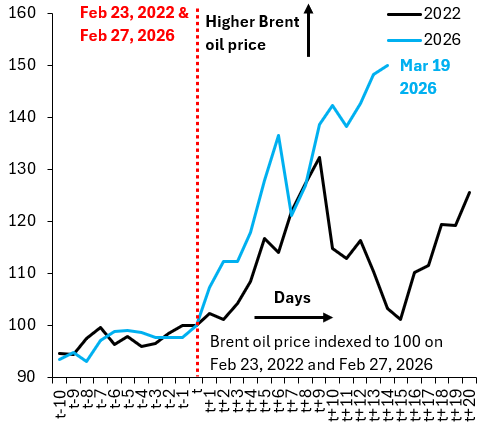

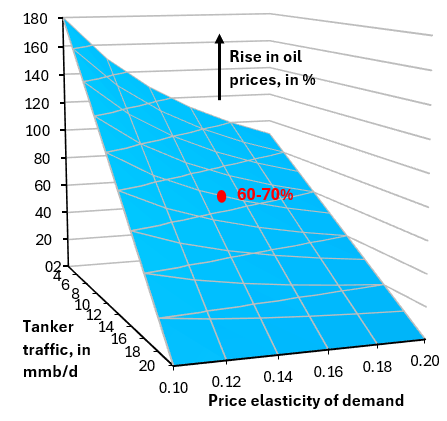

Whether or not an embargo would cause a material additional spike in oil prices depends critically on what’s now priced into oil. I think about this in two ways. First, the chart above shows the evolution of Brent since the war with Iran started (blue) and compares this – in event time – with Russia’s 2022 invasion of Ukraine (black). Before hostilities began, roughly 20 million barrels of oil transited the Strait of Hormuz daily. Russia exports around seven million barrels of oil per day. So the current shock is roughly three times as big for the oil market as 2022, which is roughly what markets now price. Second, oil out of the Persian Gulf is currently running close to ten million barrels per day, so the shortfall from before the war is ten million barrels. As I showed in yesterday’s post, reasonable assumptions for the price elasticity of demand mean this kind of shortfall implies a 60 – 70 percent rise in oil prices, which is roughly what we’ve gotten. The red dot in the chart below shows where we currently are relative to a range of assumptions for oil volumes and the elasticity. It’s hard to see Brent going to $200 unless oil out of the Persian Gulf goes back to near zero.

The bottom line is that a big risk premium is now priced in oil prices, some of which no doubt reflects the possibility of an embargo. A blockade of Iran’s ports might thus not spike oil prices all that much, even as it would send Iran into deep financial crisis. There’s no guarantee this would get the mullahs to stop fighting, but it’s really hard to wage war when your economy is imploding.