TL;DR

Supply Offers: SK Hynix is reportedly weighing buyer financing proposals tied to future AI memory supply. Funding Mechanism: Some proposals could fund production lines, equipment, or EUV tools rather than only future chip purchases. Capacity Stakes: Capacity-backed deals could help hyperscalers secure output while leaving smaller buyers with later delivery slots. Supplier Tradeoff: SK Hynix would have to balance expansion funding against flexibility over future allocation.

SK Hynix is reportedly weighing buyer financing proposals tied to future memory supply as AI infrastructure demand keeps tightening access to advanced chips. Big Tech customers are described as part of the push, which would move talks beyond ordinary procurement and into direct support for future capacity.

Some proposal paths could involve funding new production lines, helping pay for expensive semiconductor equipment, or extending support to EUV tools. Buyers exploring those options would be reaching into expansion costs and scheduling instead of waiting for finished chips to reach the market.

How the Financing Proposals Go Beyond Ordinary Chip Deals

Ordinary supply contracts settle price, volume, and delivery timing. Capacity-backed deals reach further upstream, and the current offers to secure memory supply would fit that model because they put money behind production rather than only future purchase commitments. Customer funding could shape tool orders, line priorities, construction timing, qualification work, and the amount of capacity left for customers outside the deal.

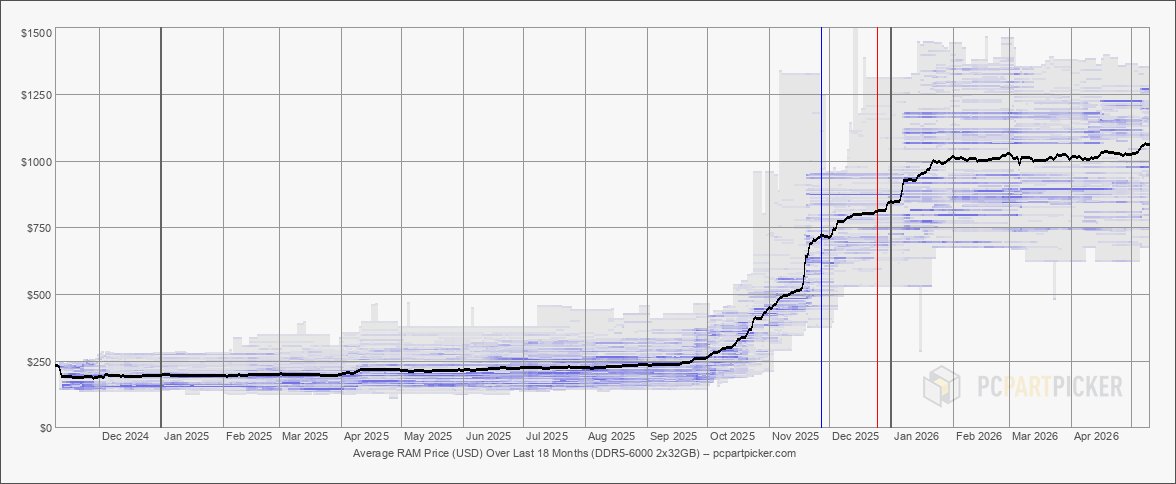

Buyer-specific commitments in early 2026 showed major AI customers moving toward tighter vendor-specific arrangements when advanced memory became harder to replace. The buyer-specific memory commitments are part of a broader pattern. Pressure had already been visible in ahyperscaler-driven memory shortage, as large customers are chasing stronger supply guarantees.

SK Hynix still has reasons to protect flexibility. Outside funding could ease expansion costs, but terms that steer output toward one buyer class, region, or product cycle could limit how freely the company allocates supply later. A narrow deal could solve a tool-purchase gap without handing over long-term allocation control, while a broader arrangement could make the customer a de facto partner in expansion choices.

Why Scarcity Is Changing Buyer Behavior

Large AI operators can justify deeper commitments because memory bottlenecks threaten far more than a single component order. Delayed HBM shipments can slow server deployment, strand accelerator purchases, and push back cloud capacity that customers plan to sell onward to developers and enterprises. HBM’s stacked design also makes it difficult to treat as a commodity substitute when a deployment plan has already been built around a specific accelerator platform.

Rare financial backing to SK Hynix fits that logic because customers traditionally purchase components rather than fund manufacturing expansion. Claim status remains reported rather than confirmed, but it describes a buyer mindset: ordinary purchase orders may not feel sufficient when production slots appear scarce. Financing becomes a way to reduce exposure to the next allocation cycle, not merely a way to negotiate price.

Conditions look harsher if available production capacity appears effectively exhausted as customers cannot afford to miss an AI rollout window. Pressure on HBM has already spilled into adjacent products, and earlier in 2026 the shift toward AI-oriented memory output was already squeezing other parts of the DRAM market.

Smaller Buyers Face the Spillover

Smaller buyers face a different version of the squeeze. Hyperscalers can answer scarcity with capital, longer planning cycles, and vendor-specific negotiations, while server manufacturers, enterprise integrators, and downstream cloud tenants are more likely to face higher prices, later delivery slots, or reduced access. A company that misses one allocation window may seek a deeper supply relationship in the next round, leaving the rest of the market with a smaller residual pool of memory.

Those downstream effects can show up outside the headline AI market. Server vendors may have processors and networking parts ready while waiting for memory. Cloud tenants may see capacity arrive later than planned if their providers cannot secure enough HBM-backed systems. Enterprise integrators can also face uncertainty when quoted delivery windows depend on memory allocations controlled by a few large buyers.

Historical Deals Show the Lock-In Path

In 2025, earlier supply lockups showed customers already willing to trade flexibility for guaranteed access. Current proposals differ because they may reach expansion itself, not just priority in the queue for finished chips. That shift would move buyer influence from procurement into the supplier’s capital planning.

March 2026 DRAM pressure also shows why the latest proposals could matter even if they do not become contracts. Once vendors start redirecting more memory output toward AI demand, procurement stops looking like a short-term pricing problem and starts looking like a structural allocation contest that favors the largest and wealthiest customers. Financing would pull buyers deeper into that contest by giving them a stake in which capacity gets built first.

Standard purchase orders leave the supplier responsible for capital spending and production sequencing. Capacity funding blurs that division. Buyers gain a stronger claim on future production, while SK Hynix has to decide whether extra capital offsets the loss of optionality that comes with customer-specific expansion.

Equipment Funding Changes the Capacity Clock

New line funding and equipment support affect different parts of expansion. A new line points to construction, process qualification, staffing, and yield ramping, while equipment support targets machinery bottlenecks that can slow advanced memory output. EUV support is narrower still because it focuses on high-cost tools that may determine which product generation receives priority.

Equipment support also changes who absorbs schedule risk. If a funded tool arrives late or qualifies slowly, buyers may expect priority treatment even though the delay sits inside the manufacturing process. SK Hynix would need terms that keep financing support from becoming an open-ended delivery promise.

Money committed to a line does not create shippable memory until tools arrive, processes qualify, and yields stabilize. A financing proposal that ignores those steps may buy influence without solving the timing problem that made the buyer seek access in the first place. Milestones would have to distinguish funding access from delivery guarantees, because support for equipment does not automatically create usable supply.

Financing Terms Would Need Guardrails

Customer support would need to distinguish capital assistance from capacity control. A payment for tools could be structured as prepayment, investment, equipment financing, or another commercial mechanism, but each version changes what the buyer can reasonably expect in return. SK Hynix would have to decide how much visibility it gives buyers into tool timing, yield ramp, and output allocation.

Governance details could decide whether the arrangement stays manageable because vague promises can turn expansion help into a future priority dispute. SK Hynix can accept help with expansion while keeping product mix, regional allocation, and customer prioritization under its own control. Any deal would also have to define what happens if demand cools, a product generation changes, or another customer needs capacity first, signaling whether SK Hynix is selling access to a project milestone or accepting a broader strategic tie.

What SK Hynix Must Balance Next

SK Hynix used its GTC 2026 AI memory showcase to emphasize its role in the AI memory market earlier in 2026. March positioning does not confirm the current talks, but it helps explain why customers would target SK Hynix rather than a less central supplier if they want to lock in advanced output. Capacity negotiations would involve a supplier whose roadmap is already framed around AI memory.

A financing partner could become important enough to influence expansion priorities, yet memory demand can shift across cloud platforms, server vendors, and product cycles. Keeping future output flexible gives SK Hynix more room to respond if one buyer slows spending or another market suddenly needs capacity. HBM, server DRAM, mobile memory, and PC memory do not move in identical cycles, so early over-commitment remains a strategic risk.

Binding the offers to secure memory supply would force SK Hynix to decide how much new capacity stays broadly allocable and how much turns into bargaining ground for the next wave of AI infrastructure demand.