Goldman Sachs has raised its target price for ASML Holding to 1,600 euros and reiterated a Buy rating. The year-to-date performance of ASML lags behind its peers, with the valuation underestimating its long-term potential. As global AI infrastructure investment accelerates, demand for EUV lithography equipment in AI chips continues to grow. Additionally, the increase in equipment volume due to global factory decentralization and the rise in chip layers are expected to drive the company’s earnings beyond expectations, with significant upside potential for the stock.

Global AI infrastructure investment continues to exceed expectations, with the semiconductor equipment sector recording robust gains overall. However, ASML Holding, as the leader in the lithography segment, has seen its year-to-date increase of approximately 45% significantly lag behind peers, creating a notable divergence between market pricing and its underlying fundamental resilience.

Goldman Sachs’ latest research report raised ASML Holding’s 12-month target price to 1,600 euros (with a bull case scenario seeing it at 2,000 euros), reiterating a buy rating. Historically, the company commanded a valuation premium of about 20% compared to peers, but its current valuation stands at only the 10th percentile of its five-year range, clearly mismatched with the acceleration of AI growth and its strengthened monopoly in EUV technology.

The report highlights that market pricing for three key drivers — AI-driven EUV revenue, incremental demand for equipment due to inefficiencies in the manufacturing process, and the continued increase in EUV layers — remains overly conservative. Under the base-case scenario, these assumptions are above the market-implied levels, with a risk-reward ratio tilted positively by a factor of 2, indicating significantly greater upside potential than downside risk.

The report highlights that market pricing for three key drivers — AI-driven EUV revenue, incremental demand for equipment due to inefficiencies in the manufacturing process, and the continued increase in EUV layers — remains overly conservative. Under the base-case scenario, these assumptions are above the market-implied levels, with a risk-reward ratio tilted positively by a factor of 2, indicating significantly greater upside potential than downside risk.

Looking ahead, three catalysts are worth monitoring: first, following the completion of the GAA architecture transition, an update to the process node roadmap could serve as a leading indicator for further increases in EUV layers; second, rising design orders from laggard manufacturers would validate the diffusion of EUV demand from a single customer to multiple customers; third, the accelerated deployment of enterprise-level AI (especially Agentic AI) may further boost capital expenditure expectations.

Valuation discount relative to peers is unsustainable.

ASML Holding’s current valuation discount is not justified, as its fundamental strengths remain underappreciated by the market.

Year-to-date, ASML Holding’s share price increase has significantly lagged behind the approximately 60% gain of the European tech hardware sector overall and also trails major semiconductor equipment peers: ASM International, BESI, Applied Materials, Lam Research, and KLA Corp recorded gains of approximately 70%, 95%, 70%, 70%, and 55%, respectively.

From a valuation perspective, ASML historically enjoyed a premium of about 20% over global semiconductor equipment peers, but now trades at a slight discount, standing at the 10th percentile of its five-year range. This discount is clearly misaligned with the company’s accelerating AI business, expanding exposure to advanced memory chips, and its increasingly fortified competitive moat (a de facto monopoly in EUV lithography).

Accelerated AI infrastructure investment drives structural uplift in EUV demand.

Market skepticism regarding the sustainability of AI demand is gradually receding, with recent data from cloud providers and supply chains pointing to a more optimistic outlook. Goldman Sachs recently revised upward its forecast for wafer fab equipment (WFE) spending, providing significant quantitative support for a bullish view on ASML.

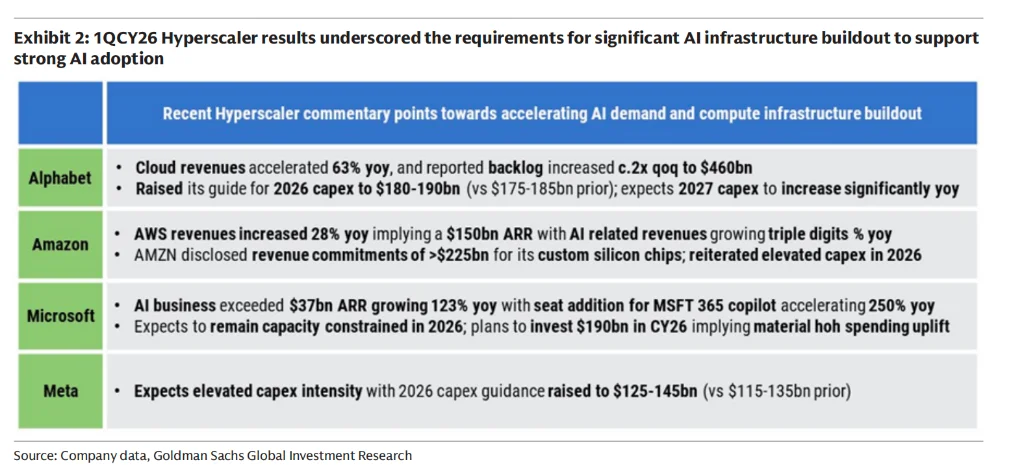

First, the resilience of capital expenditures by hyperscale cloud vendors continues to be validated. Google’s AI revenue in the first quarter grew 63% year-over-year, with its order backlog doubling sequentially to $460 billion; Amazon Web Services (AWS) revenue increased 28% year-over-year, marking the fastest growth in nearly 15 quarters, with AI-related revenue maintaining triple-digit growth.

A more critical signal comes from Alphabet, which raised its capital expenditure guidance for 2026 to between $180 billion and $190 billion and explicitly stated that spending in 2027 will be significantly higher, effectively alleviating market concerns about a peak in 2026 capital expenditures. Based on these trends, capital expenditures by hyperscale cloud vendors are expected to grow from $720 billion in 2026 to $918 billion in 2027 and $1.02 trillion in 2028, corresponding to growth rates of 28% and 11%, respectively.

Secondly, semiconductor supply chains are also signaling heightened tension. Taiwan Semiconductor noted in its Q1 earnings call that the supply-demand gap for advanced AI chips remains highly strained, with the company actively expanding capacity; Samsung indicated that fulfillment rates are at historical lows, with some customers already releasing demand for 2027 ahead of schedule.

Against this backdrop, global front-end equipment spending forecasts have been revised upward accordingly. Global WFE market size is projected to reach $141 billion in 2026 and $186 billion in 2027, representing year-over-year growth of 28% and 32%, respectively, both higher than previous estimates of $132 billion and $160 billion.

Finally, focusing on ASML Holding’s EUV business, the contribution of AI is expected to continue rising. Current estimates suggest that AI-related revenue as a proportion of EUV will reach the high 20% range by 2027, while the current stock price reflects only the mid-20% range; under a bullish scenario, this proportion could rise to the mid-30% range. Overall, between 2025 and 2027, AI demand is expected to contribute approximately 40% of incremental EUV tool demand under a base-case scenario and around 50% under a bullish scenario.

Structural inefficiencies in customer markets: Incremental equipment demand driven by globally dispersed factory construction is underestimated.

Structural inefficiencies in customer markets: Incremental equipment demand driven by globally dispersed factory construction is underestimated.

Simultaneous global expansion by multiple wafer fabs will drive higher total wafer starts, thereby increasing demand for lithography tools, but this logic is not yet fully reflected in the current stock price.

The current stock price implies only about 7% of incremental demand stemming from manufacturing inefficiencies, while the target price corresponds to 8%, already approaching the upper limit of ASML Holding’s own guidance range (5%-8%). Though the gap seems small, considering ASML Holding’s substantial revenue base, the absolute amount represented by this difference is quite significant.

Samsung is the key catalyst for the realization of this logic. The company has recently released multiple positive signals: strong momentum for customer orders at the 2nm process node; evaluating the construction of a second wafer fab in Taylor, Texas; and explicitly stating in its Q1 2026 earnings report that equipment expenditures will increase significantly as new capacity deployment progresses. Additionally, Samsung noted that fulfillment rates are at historical lows, with some customers already releasing 2027 demand ahead of schedule, further confirming the urgency of capacity expansion.

More broadly, if leading wafer fabs such as Samsung, aside from Taiwan Semiconductor, can achieve scaled production in advanced process technologies, it will break the pattern previously dominated by a single manufacturer. Parallel expansions by globally distributed leading-edge wafer fabs imply that achieving the same capacity will require more equipment investment (i.e., manufacturing inefficiencies), driving higher total wafer start requirements, a structural change that has yet to be fully priced in by the market.

Increase in EUV layers: Conservative technology penetration trajectory; even if new technologies are delayed, the profit impact remains positive.

The current share price reflects a technology penetration pace still at the lower end of ASML Holding’s own guidance. ASML Holding’s official target for 2030 is 25-30 layers for logic chips and 7-10 layers for memory chips (currently around 5 layers for memory). Under bearish, current, and bullish scenarios, logic chips correspond to 22, 23, and 25 layers respectively, while memory chips are expected to add 2, 2, and 3 layers respectively.

Even if the next-generation lithography technology (high NA) is delayed, customers may purchase more existing low NA equipment to compensate for capacity. Existing equipment has higher profit margins, and selling more will help boost ASML Holding’s earnings per share (EPS). The target price assumes 24 EUV layers for logic chips by 2027, slightly above the 23 layers implied by the current share price. The previous assumption of 25 layers was revised downward due to a major customer’s cautious stance on high NA, but the marginal increase in low NA shipments still positively impacts EPS.

Several catalysts over the coming quarters are expected to drive ASML Holding’s share price higher: The transition to GAA architecture is projected to be largely completed by the end of 2026, with updates to the node scaling roadmap serving as a leading indicator for the inflection point in EUV layer growth; historically lagging players securing more design orders will further validate the multi-customer landscape; and accelerated enterprise AI adoption (particularly CPU and HBM demand driven by Agentic AI) may lead to upward revisions in capital expenditure expectations.

Editor/Stephen