State pension age must be pushed back to 74 years old to maintain the annual payment rate hike provided by the triple, a leading think tank has warned.

The Institute of Fiscal Studies (IFS) is calling for greater scrutiny of the retirement benefit, previously revealing that the triple lock pension policy has cost the government an additional £11billion annually since its introduction in 2011.

Its recent Pensions Review report stated: “eIncreases in the state pension age required to keep spending on the state pension below a certain level of national income would have to be substantial.

“[Official] modelling shows that to keep public spending on the state pension below 6 per cent of nation income while retaining the triple lock, the state pension age would have to rise to 69 by 2049 and 74 by 2069.”

The state pension age should be “pushed back” to 74, analysts claim

GETTY

In an earlier report, the IFS determined the state pension would be approximately 11 per cent lower than its current value without the triple lock in place.

The policy has significantly increased state financial support to pensioners beyond what would have been provided through traditional indexation methods.

According to the IFS findings, a full new state pension currently represents 25 per cent of full-time mean earnings for existing claimants.

If the policy continues indefinitely, the IFS projects that by 2050 the state pension could range between 26 per cent and 32 per cent of mean full-time earnings.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

The state pension age is rising GETTY

The state pension age is rising GETTY

In today’s terms, this translates to an annual income between £10,900 and £13,400 – a difference of £2,500 per year.

The IFS warns that generating an additional £2,500 annually from state pension age would require savings of at least £50,000-£60,000 today, making retirement planning increasingly challenging for individuals.

It calculates that additional spending on the state pension due to the triple lock could range between £5billion and £45billion annually by 2050 in today’s terms.

Furthermore, the think tank notes that this uncertainty accounts for the growing pensioner population and represents spending above what would occur under earnings indexation alone.

Analysts note that such unpredictability makes future Government financial planning significantly more difficult, with the potential for dramatic variations in required public expenditure over the coming decades.

Mike Ambery, the retirement savings director at Standard Life, warned that the state pension age could be pushed back further to maintain affordability.

LATEST DEVELOPMENTS:

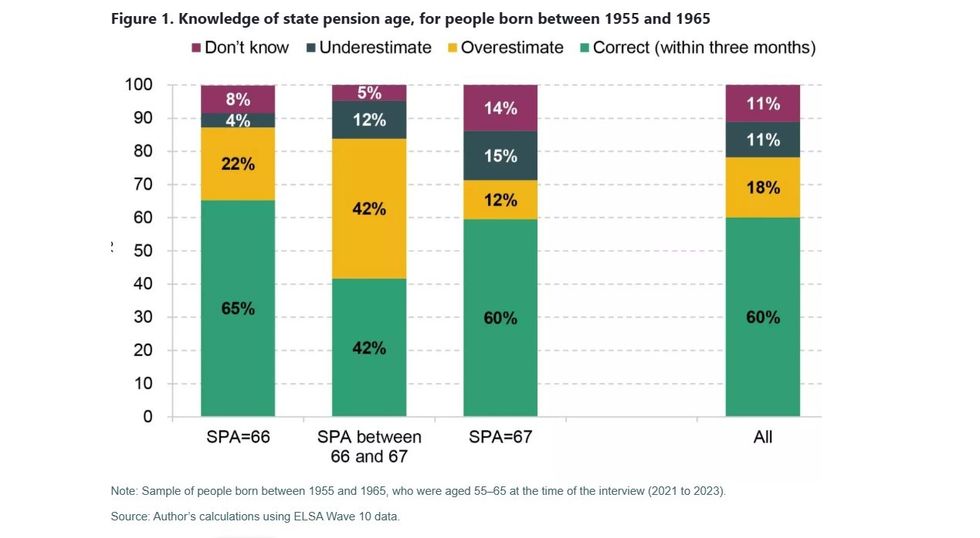

The IFS’s research into the state pension age suggests thousands of Britons lack essential knowledge of looming changes IFS

The IFS’s research into the state pension age suggests thousands of Britons lack essential knowledge of looming changes IFS

“With the state pension accounting for a significant proportion of all welfare spending, the report highlights the risk that the state pension age could be pushed back further to maintain affordability,” he said.

Ambery noted that people’s ability to continue working has not kept pace with increases in state pension age.

He pointed to rising poverty levels among those in their early 60s as evidence of this growing disconnect.

The IFS expressed concern that controlling pension costs through age increases would particularly impact those expecting poor health, those unable to remain in employment, and those less likely to enjoy extended retirement years.