Apr 18, 2025

IndexBox has just published a new report: United Kingdom – Ball and Roller Bearings – Market Analysis, Forecast, Size, Trends And Insights.

Driven by rising demand, the bearing market in the UK is expected to see a slight increase in performance over the next decade. The market is projected to have a CAGR of +1.1% in volume and +1.6% in value from 2024 to 2035, indicating positive growth in the industry.

Market Forecast

Driven by rising demand for bearing in the UK, the market is expected to start an upward consumption trend over the next decade. The performance of the market is forecast to increase slightly, with an anticipated CAGR of +1.1% for the period from 2024 to 2035, which is projected to bring the market volume to 18K tons by the end of 2035.

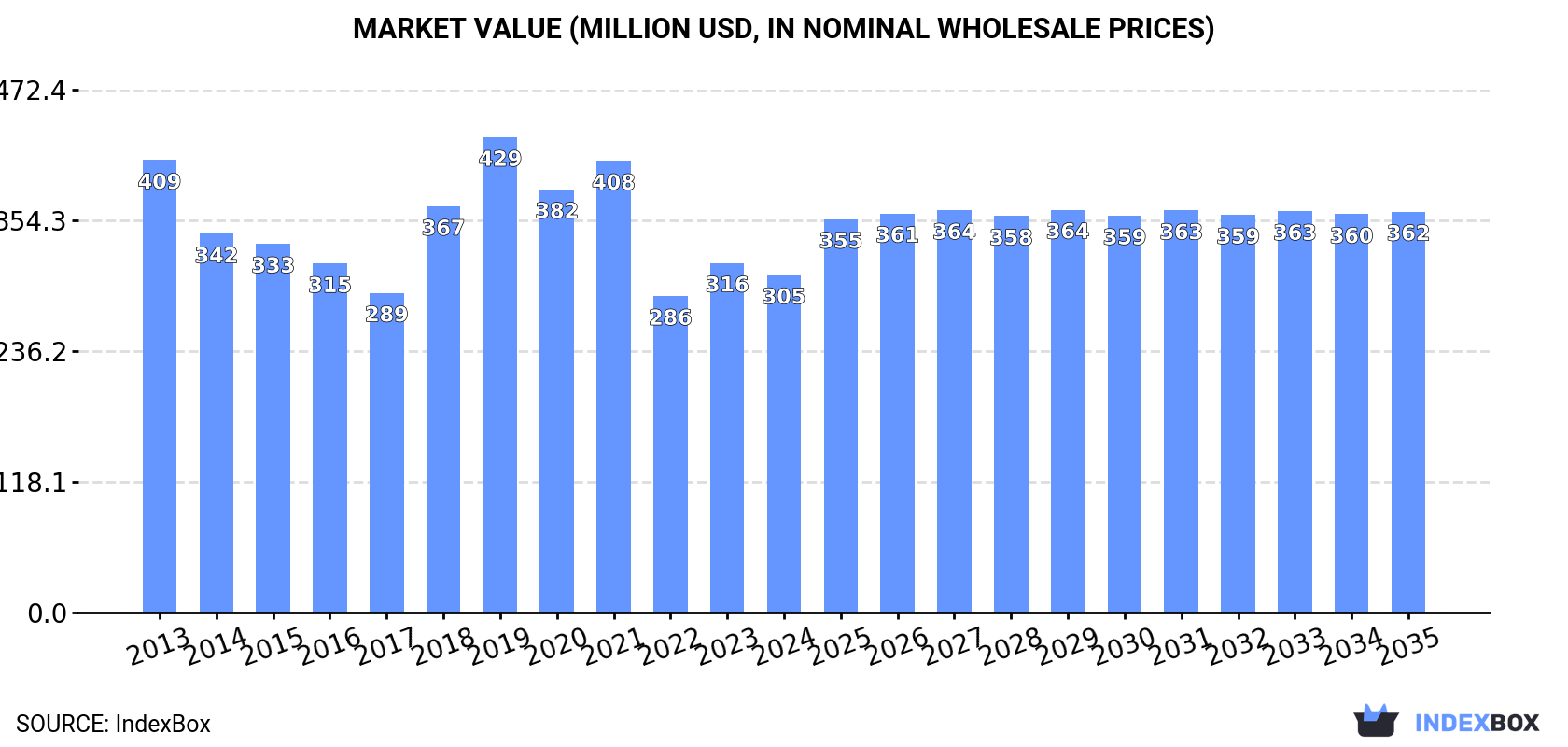

In value terms, the market is forecast to increase with an anticipated CAGR of +1.6% for the period from 2024 to 2035, which is projected to bring the market value to $362M (in nominal wholesale prices) by the end of 2035.

ConsumptionUnited Kingdom’s Consumption of Ball and Roller Bearings

ConsumptionUnited Kingdom’s Consumption of Ball and Roller Bearings

In 2024, bearing consumption in the UK surged to 16K tons, increasing by 19% on the previous year. In general, consumption, however, showed a abrupt decline. Over the period under review, consumption hit record highs at 32K tons in 2013; however, from 2014 to 2024, consumption failed to regain momentum.

The revenue of the bearing market in the UK shrank slightly to $305M in 2024, declining by -3.4% against the previous year. This figure reflects the total revenues of producers and importers (excluding logistics costs, retail marketing costs, and retailers’ margins, which will be included in the final consumer price). Over the period under review, consumption, however, showed a noticeable setback. Over the period under review, the market hit record highs at $429M in 2019; however, from 2020 to 2024, consumption remained at a lower figure.

ProductionUnited Kingdom’s Production of Ball and Roller Bearings

Bearing production in the UK fell slightly to 11K tons in 2024, which is down by -2.3% against 2023. Over the period under review, production recorded a pronounced reduction. The most prominent rate of growth was recorded in 2023 when the production volume increased by 4.9% against the previous year. Over the period under review, production hit record highs at 18K tons in 2013; however, from 2014 to 2024, production failed to regain momentum.

In value terms, bearing production contracted to $331M in 2024 estimated in export price. Overall, production showed a noticeable decline. The most prominent rate of growth was recorded in 2019 when the production volume increased by 14%. Bearing production peaked at $527M in 2013; however, from 2014 to 2024, production stood at a somewhat lower figure.

ImportsUnited Kingdom’s Imports of Ball and Roller Bearings

In 2024, the amount of ball and roller bearings imported into the UK fell modestly to 14K tons, which is down by -2.5% against the year before. Over the period under review, imports recorded a deep slump. The most prominent rate of growth was recorded in 2021 with an increase of 25% against the previous year. Over the period under review, imports reached the peak figure at 35K tons in 2013; however, from 2014 to 2024, imports remained at a lower figure.

In value terms, bearing imports fell to $385M in 2024. Overall, imports continue to indicate a pronounced contraction. The growth pace was the most rapid in 2021 with an increase of 25%. Imports peaked at $498M in 2014; however, from 2015 to 2024, imports failed to regain momentum.

Imports By Country

China (2.7K tons), Germany (1.8K tons) and Italy (1.6K tons) were the main suppliers of bearing imports to the UK, together accounting for 45% of total imports. Japan, France, India, the United States, Poland, Romania, Belgium and the Netherlands lagged somewhat behind, together comprising a further 42%.

From 2013 to 2024, the biggest increases were recorded for India (with a CAGR of +16.8%), while purchases for the other leaders experienced mixed trend patterns.

In value terms, Germany ($83M), the United States ($77M) and France ($39M) appeared to be the largest bearing suppliers to the UK, together accounting for 52% of total imports. China, Italy, Japan, Romania, Belgium, India, Poland and the Netherlands lagged somewhat behind, together comprising a further 35%.

In terms of the main suppliers, India, with a CAGR of +20.3%, saw the highest rates of growth with regard to the value of imports, over the period under review, while purchases for the other leaders experienced more modest paces of growth.

Import Prices By Country

In 2024, the average bearing import price amounted to $28,351 per ton, with a decrease of -6.9% against the previous year. In general, import price indicated a remarkable increase from 2013 to 2024: its price increased at an average annual rate of +6.5% over the last eleven years. The trend pattern, however, indicated some noticeable fluctuations being recorded throughout the analyzed period. Based on 2024 figures, bearing import price increased by +27.9% against 2018 indices. The most prominent rate of growth was recorded in 2014 an increase of 60%. The import price peaked at $30,457 per ton in 2023, and then reduced in the following year.

Prices varied noticeably by country of origin: amid the top importers, the country with the highest price was the United States ($127,992 per ton), while the price for Poland ($11,284 per ton) was amongst the lowest.

From 2013 to 2024, the most notable rate of growth in terms of prices was attained by Germany (+11.3%), while the prices for the other major suppliers experienced more modest paces of growth.

ExportsUnited Kingdom’s Exports of Ball and Roller Bearings

In 2024, shipments abroad of ball and roller bearings decreased by -27.4% to 8.4K tons, falling for the second consecutive year after two years of growth. Over the period under review, exports continue to indicate a abrupt curtailment. The most prominent rate of growth was recorded in 2022 when exports increased by 13% against the previous year. The exports peaked at 23K tons in 2014; however, from 2015 to 2024, the exports remained at a lower figure.

In value terms, bearing exports contracted to $412M in 2024. In general, exports continue to indicate a noticeable shrinkage. The pace of growth appeared the most rapid in 2022 when exports increased by 13%. The exports peaked at $633M in 2014; however, from 2015 to 2024, the exports stood at a somewhat lower figure.

Exports By Country

Belgium (2.2K tons), Germany (1.9K tons) and the Netherlands (1.6K tons) were the main destinations of bearing exports from the UK, together comprising 69% of total exports.

From 2013 to 2024, the most notable rate of growth in terms of shipments, amongst the main countries of destination, was attained by Germany (with a CAGR of +2.2%), while the other leaders experienced a decline.

In value terms, Belgium ($79M), the United States ($68M) and Germany ($48M) constituted the largest markets for bearing exported from the UK worldwide, with a combined 47% share of total exports. The Netherlands, China, France, India, Spain, the Czech Republic and Ireland lagged somewhat behind, together accounting for a further 28%.

In terms of the main countries of destination, China, with a CAGR of +5.8%, recorded the highest growth rate of the value of exports, over the period under review, while shipments for the other leaders experienced mixed trend patterns.

Export Prices By Country

In 2024, the average bearing export price amounted to $49,050 per ton, growing by 27% against the previous year. In general, export price indicated moderate growth from 2013 to 2024: its price increased at an average annual rate of +4.7% over the last eleven-year period. The trend pattern, however, indicated some noticeable fluctuations being recorded throughout the analyzed period. Based on 2024 figures, bearing export price increased by +61.6% against 2021 indices. The growth pace was the most rapid in 2023 when the average export price increased by 27%. Over the period under review, the average export prices reached the maximum in 2024 and is expected to retain growth in years to come.

There were significant differences in the average prices for the major foreign markets. In 2024, amid the top suppliers, the country with the highest price was the United States ($195,006 per ton), while the average price for exports to Germany ($24,835 per ton) was amongst the lowest.

From 2013 to 2024, the most notable rate of growth in terms of prices was recorded for supplies to China (+15.4%), while the prices for the other major destinations experienced more modest paces of growth.

Source: IndexBox Market Intelligence Platform