For years, the debate around active versus passive investing has raged on. And over the past decade, passive strategies have gained popularity thanks to their simplicity, low costs and strong performance as markets have climbed to record highs. While, for some, this performance has strengthened the case against active investing, it is also a double-edged sword.

Markets, such as tides, are constantly shifting. Active strategies navigate these shifts with intent, while passive portfolios are bound to the current – leaving them vulnerable to choppier waters. Investment manager Orbis believes the next decade could be very challenging for those invested solely in passive and/or traditional strategies unless they adjust their portfolios.

So, what’s clouding the once-clear waters of passive investing?

Why rising concentration and soaring valuations spell trouble

First, markets are more concentrated than ever. While markets have performed well over the past decade, most of the gains have come from a handful of stocks. As a result, indices – and subsequently passive strategies – are now heavily reliant on a small number of mega-cap technology stocks. For example, the top companies in the S&P 500 index account for roughly 40 per cent of the index’s market capitalisation1. This poses a clear risk for passive investors. Should the fortunes of these mega-cap stocks reverse, passive portfolios could face significant headwinds.

Second, valuations – particularly in the US – are circling historic highs, driven by near-record profit margins and expectations of robust earnings growth. This leaves markets highly vulnerable to a reversal, as even slight disappointments in earnings could trigger sharp declines. Typically, this setup (high market concentration and valuations), doesn’t bode well for the future returns of passive equity strategies.

One other issue is when the market turns. History tells us that the most expensive areas fall the fastest and furthest (see table below). In Orbis’s view, the sections of the market that have delivered the best returns over the past 10 years are unlikely to deliver again, and instead, they present more significant downside risk. So, what can passive investors do to balance their portfolios?

Source: LSEG Datastream, Orbis. Relative returns are calculated geometrically and annualised. AI: Artificial Intelligence. Data as at 30, June 2025

Blending active and passive

One approach is to blend passive and active strategies. Unlike their counterparts, active strategies can navigate challenging environments with intent, lending passive portfolios an extra degree of resilience. Passive strategies are inherently vulnerable to turns in sentiment, when they are obliged to sell in lockstep. But active strategies are not forced to sell in the same way. Active managers can buy on conviction when stock prices fall – rather than selling on weakness as market-cap-weighted passive strategies inevitably do.

That’s not to say that passive strategies have no place in a portfolio. This is not a zero-sum game; passive has advantages over active strategies when it comes to cost and convenience, and passive strategies can be used as an efficient means of achieving core exposures. Moreover, the performance of passive and active strategies tends to run in cycles, with one approach outperforming the other for some time before the ascendancy reverses.

But a combination of active stock-picking and passive core holdings can provide a crucial balance that helps investors to steer their way through challenging and polarised market environments. But that’s just one layer.

Is the active portion truly diversified?

When they look beyond passive indices, investors should also be thinking about funds and strategies that stand out from the herd and complement their existing holdings/exposure. That way, they can hope to achieve diversification through investment style as well as by asset class. Funds with a distinctive investment approach are less likely to be correlated with generic passive approaches, and investors should be careful to ensure that their managers are taking a genuinely active approach rather than tightly hugging indices with just a nominal active share.

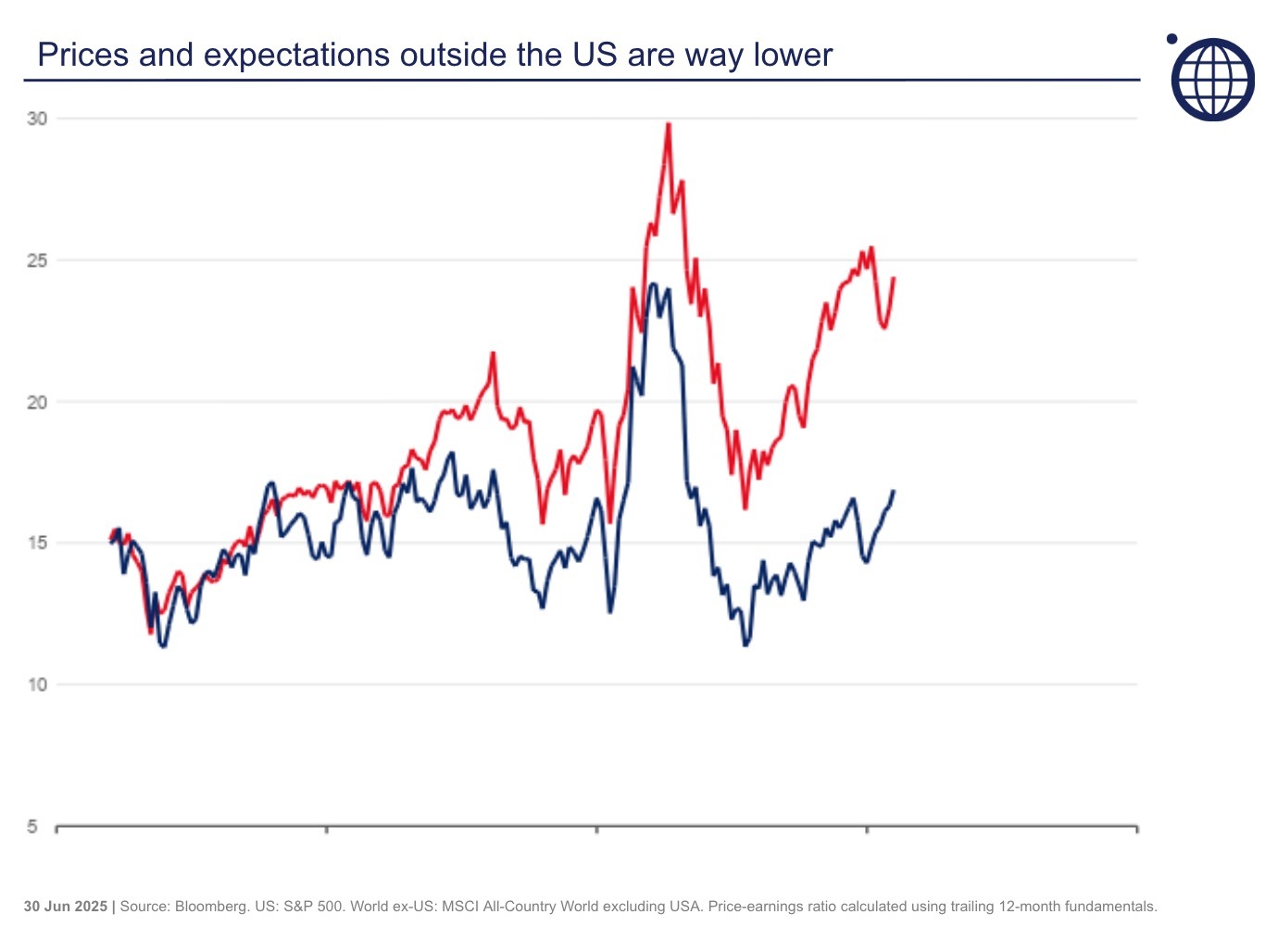

The same goes for regional exposures and underlying holdings. While gains have been concentrated in a handful of stocks – leaving limited opportunities for broader outperformance – this also creates an opportunity for active investors who are willing to take the road less travelled. As the US market has continued to attract the bulk of the world’s capital, this sustained demand has led to a historically wide gap between the average US-listed stock and the rest of the world.

Source: Bloomberg US: S&P 500. World ex-US: MSCI All Country World excluding USA. Price-earnings ratio calculated using trailing 12-month fundamentals. Data as at 30, June 2025

Such a dislocation provides active managers with an opportunity to find overlooked gems with the potential to generate sustainable returns and provide genuine diversification. By adding an active manager who zigs when their passive portfolio zags, investors can reduce the risk and volatility within their overall portfolio.

In a world of highly concentrated markets, still-high inflation and heightened correlations, diversification is harder to come by. But achieving appropriate diversification is by no means impossible. By blending active and passive strategies and seeking out opportunities with low correlations to the broad markets and their existing holdings, investors can create portfolios that are more resilient and better balanced – leaving them well positioned to navigate the choppy waters more smoothly.

Click here to find out more about Orbis Investments

1 Source: https://www.apolloacademy.com/extreme-concentration-in-the-sp-500-2/

Capital at risk.

Approved for issue in the United Kingdom by Orbis Investments (U.K.) Limited, which is authorised and regulated by the Financial Conduct Authority. Orbis Investments (U.K.) Limited is incorporated in England & Wales under company number 8138002. Registered office address: 28 Dorset Square, London, NW1 6QG.