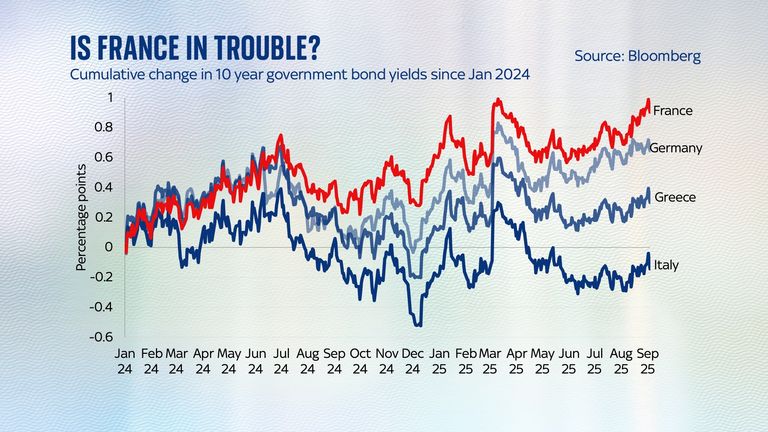

Once upon a time if folks wanted to pinpoint the most economically-vulnerable country in Europe – the one most likely to face a crisis – they would invariably point to Greece or to Italy.

They were the nations with the eye-wateringly high bond yields, signalling how reluctant financiers were to lend them money.

Today, however, all of that has changed. The country invariably highlighted as Europe’s problem child is France.

Indeed, look at the interest rates investors charge European nations and France faces even higher interest rates than Greece.

And these economic travails are central to understanding the political difficulties France is facing right now, with one prime minister after another resigning in the face of a parliamentary setback.

Read more:

French PM looks set to lose confidence vote

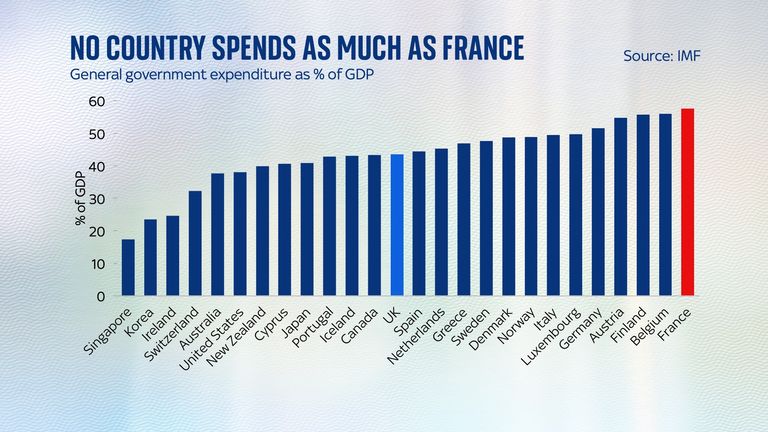

It mostly comes back to the state of the public finances. France’s deficit is among the highest in the developed world right now.

Everyone spent enormous sums during the pandemic. But France has struggled, more than nearly everyone else, to bring its spending back down and, hence, to reduce its deficit. Successive budget plans have been announced and then shelved in the face of political resistance.

France’s government spends more, as a percentage of gross domestic product, than any other developed economy.

The government’s most recent budget plans called for what most people would see as relatively minor spending cuts – barely more than a couple of percentage points off spending, after which France would still be the third biggest spender in the world.

But even these cuts were too controversial for the French people, or rather their politicians.

Yet another prime minister looks likely to fall victim to an unsuccessful bill. Deja vu all over again, you might say.

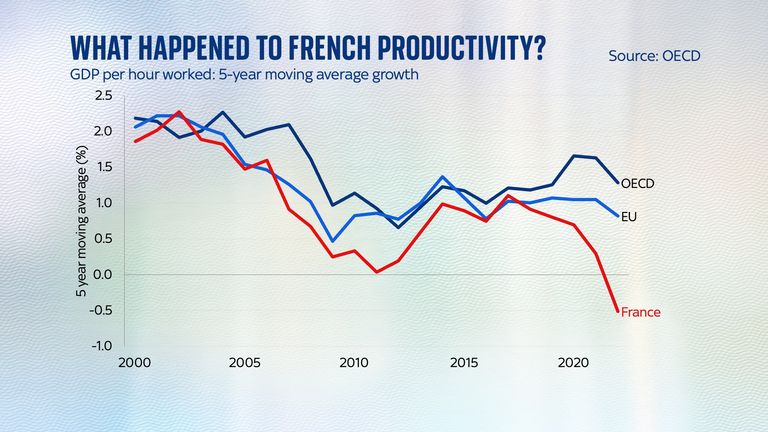

A deeper issue is that the latest worsening in France’s public finances isn’t just a sign of political resistance, or indeed of a nation that can’t bear to take the unpalatable fiscal medicine others (for instance Greece or the UK) have long been ingesting.

For years, France could rely on a phenomenon many other developed economies couldn’t: strong productivity growth.

The country’s people might not work as many hours as everyone else, but they sure created a lot of economic output when they were at their desks.

However, in recent years, French productivity has disappointed. Indeed, output per hour growth in France has dropped well below other nations, which in turn means less tax revenue and, lo and behold, the deficit gets bigger and bigger.

All of which is why so many people, including Prime Minister Francois Bayrou himself, have warned that France is at risk of a market meltdown.

In a recent speech, he pointed to the example of Liz Truss and her 2022 mini-Budget. Beware the market, he said. You never know how close you are to a crisis.