Utterly broken after investing almost $370,000 of her retirement savings into the now-collapsed First Guardian Master Fund and learning she may not get most of it back, Mel Wohlers contemplated ending her life.

“I went to a really dark place because of this and almost did something really stupid,” a tearful Ms Wohlers says before adding: “And I don’t want to.”

- Suicide Call Back Service on 1300 659 467

- Lifeline on 13 11 14

- Aboriginal & Torres Strait Islander crisis support line 13YARN on 13 92 76

- Kids Helpline on 1800 551 800

- Beyond Blue on 1300 224 636

- Headspace on 1800 650 890

- ReachOut at au.reachout.com

- MensLine Australia on 1300 789 978

- QLife 1800 184 527

Ms Wohlers is one of about 12,000 Australians haunted by the loss of more than $1 billion of retirement savings after the collapses of First Guardian and Shield.

Like Ms Wohlers, many were approaching retirement and lured in with promises of grand returns.

Some investors have lost more than $1 million. Some still have no idea they’ve been caught up.

“I think there’s a lot of older people that maybe aren’t on the internet and they don’t even know [about the super collapses],” Ms Wohlers says.

In the past decade alone, Australia’s total superannuation assets have more than doubled to about $4.3 trillion in funds under management, including $3 trillion in funds overseen by the Australian Prudential Regulation Authority (APRA).

There is now over $1 trillion in self-managed superannuation funds, which means a big chunk of money isn’t regulated by APRA, leaving the Australian Securities and Investments Commission (ASIC) as the only watchdog to protect consumers.

When it comes to First Guardian and Shield, and with people’s futures at stake, investors have accused ASIC of taking far too long to act.

ASIC says it acted as soon as it could

ASIC blocked investment in Shield in February 2024 and froze the assets of First Guardian in February this year.

This happened well after reports to the corporate watchdog of alleged misconduct as early as January 2021, in emails sent to the regulator seen by ABC News.

Do you know more?

If you have more information about this story please contact Nassim Khadem at khadem.nassim@abc.net.au or nassimkhadem@protonmail.com

ASIC deputy chair Sarah Court, who has commonly described the First Guardian and Shield cases as “industrial-scale misconduct”, says the regulator acted as soon as it could.

“We don’t think we missed red flags,” she tells ABC News ahead of ASIC’s appearance at a parliamentary hearing on Thursday, when she was grilled by politicians about whether it was a tough cop on the beat, properly identifying financial misconduct.

“There are thousands and thousands of managed investment schemes at any particular time.

“As soon as we became aware that there was something wrong with the underlying fund itself, like the solvency of the fund or investors’ monies in relation to that fund, then we acted very quickly to shut that down.”

ASIC has also separately raised serious concerns about asset manager Australian Fiduciaries, alleging inadequate management of conflicts of interest.

Another 600 investors have pumped roughly $160 million into managed investment schemes offered by Australian Fiduciaries since February 2020, predominantly through self-managed super funds (SMSFs).

Those investigations into Australian Fiduciaries are still underway, although ASIC says it has already taken court actions, such as freezing and receivership orders, against the company and a large number of related entities.

In all of these cases, no criminal charges have been laid, but ASIC is heading to court to make allegations against the people at the centre of the funds — those involved in managing and promoting the schemes.

Ms Court says the regulator has 25 active investigations into key players linked to First Guardian and Shield and has undertaken 45 separate court-related actions in an effort to protect assets, get travel restraints, have companies wound up and “try to get to the heart of what’s really gone on here”, Ms Court says.

ASIC’s allegations — yet to be tested in court — include that hundreds of millions of dollars of investor funds were sent offshore and used by the companies’ directors for pet projects.

“These two funds … were riddled with conflicts, with misconduct, with false statements that were made to investors,” Ms Court said.

‘Complex web’ but no criminal charges

The regulator is investigating almost everyone involved, including the telemarketers who first contacted investors, often using hard-sell tactics to convince them to move their superannuation savings out of APRA-regulated super funds and into managed investment schemes that do not face the same level of scrutiny.

The corporate watchdog is also investigating financial planners who often had connections with the telemarketers and who convinced the investors to sign legal documents known as Statements of Advice (SOAs) that would lock them into moving their superannuation savings — in many cases hundreds of thousands of dollars — into less regulated schemes.

Ms Court told a Parliamentary Joint Committee hearing on Thursday 140 licensed financial advisers were being examined for their role in the collapse of the Shield and First Guardian funds. She said 20 have been taken to court, 50 are under investigation and 70 more are on an ASIC follow-up list.

Ms Court tells ABC News she cannot comment on ASIC’s investigations and whether criminal charges will be laid, but notes that “the buck stops with all of those people that were involved in this”.

“We are by no means finished here,” she said.

“We have a number of very active investigations and I certainly expect more enforcement outcomes to follow.”

Ms Court says people who ran the funds — First Guardian’s David Anderson and Shield’s Paul Chiodo, as well as financial planners including Ferras Merhi — were “at the very heart of a range of the matters that we are looking at and certainly those investigations are live and continuing”.

“We are just at the beginning of the range of matters that we’re taking,” she said.

“The buck stops with all of those people that were involved in this, whether you’re an advisor, whether you are a lead generator, whether involved in the fund, whether you’re one of the trustees, whether the ratings agency, whether an auditor, whether a licence holder.

“All of these people, in our view, have got a case to answer and we are getting to the bottom of this complex web of issues but … there will be much more activity to come.”

The legal representative for Mr Anderson, Dan Mackay of Mackay Chapman lawyers, referred ABC News to previous statements that “there have been no findings of fact or law by any court or tribunal, nor by ASIC”.

He says Mr Anderson declined an interview with ABC News “as he does not want this to become a trial by media” and that he would exercise his rights in response to any allegations against him “at the appropriate time, in the appropriate forum”.

Key figures under investigation

The corporate watchdog has already frozen the assets and slapped travel bans on many of the people it is investigating. ASIC’s investigations are ongoing and no criminal charges have been laid.

David Anderson

Falcon Capital chief executive and the manager of First Guardian Master Fund.

Mr Anderson has denied wrongdoing and says he doesn’t want “trial by media”. He is under investigation by ASIC for allegedly inappropriately using investor money to pay commissions to marketing groups and for pet projects, including fine dining restaurants and a craft beer brewhouse.

Mr Anderson is alleged by ASIC to have moved hundreds of millions of dollars to offshore companies tied to him, as well as using investor cash to prop up his own businesses and make a mortgage payment on his lavish Melbourne home.

Simon Selimaj

Falcon Capital and First Guardian co-founder.

In 2013, Mr Selimaj told a Latrobe University podcast the fund was “ethical” and shariah-compliant (abiding by Islamic principles), despite later revelations First Guardian was investing in craft breweries.

His assets have been frozen by ASIC and he is under investigation. A Lamborghini worth $550,000 was found in his possession, according to the liquidator’s report. He was contacted for comment.

Paul Chiodo

Keystone Asset Management director, manager of Shield Master Fund.

Mr Chiodo has denied any wrongdoing and argues he was unfairly targeted by the regulator. ASIC says he is under investigation for allegedly inappropriately using investor money to pay commissions to marketing groups and host events with sporting stars, including former boxer Floyd Mayweather.

Keystone was also trustee of the Advantage Diversified Property Fund (ADPF), a wholesale property fund in which ASIC alleges a large proportion (more than 50 per cent, if marketing commissions are included) of Shield’s funds had been invested and which had, in turn, made loans to various companies associated with Mr Chiodo to fund luxury property development projects in Fiji, Italy, Port Douglas, and Melbourne.

Mr Chiodo says these were disclosed in the fund documents. In one case, ADPF loan funds appear to have been used to purchase a penthouse property for Mr Chiodo’s wife. Mr Chiodo says he paid for the penthouse through development management fees.

Ferras Merhi

Venture Egg chief executive. Also owns Financial Services Group Australia, which channelled investors into First Guardian and Shield.

Mr Merhi has denied any wrongdoing. He allegedly had agreements with Mr Anderson and Mr Chiodo to bring new customers into their funds. ASIC alleges he engaged in unconscionable conduct, failed to act in the best interests of clients, gave conflicted advice and provided defective statements of advice while receiving millions of dollars.

Mr Merhi told ABC News in a written statement: “Every allegation of unlawful conduct that ASIC has made, and any allegation it might yet make, will be strenuously defended in the court proceedings. Interested non-parties may apply to the court for access to the relevant documents. My substantive defence to all allegations will be set out in those court filings.”

Osama Saad

Former director of Aus Super Compare and Atlas Marketing and Ferras Merhi’s business partner.

Mr Saad denies any wrongdoing. He assisted in marketing the Shield Master Fund and First Guardian Master Fund. He is now under ASIC investigation for receiving allegedly illegal commissions.

Mr Saad told ABC News: “Every allegation of unlawful conduct that ASIC has made, and any allegation it might yet make, will be strenuously defended in the court proceedings. Interested non-parties may apply to the court for access to the relevant documents. My substantive defence to all allegations will be set out in those court filings.”

Rashid Alshakshir

Former director of Lion & Horn, Indigo Group and Nohap.

Like Mr Saad, Mr Alshakshir allegedly had agreements with David Anderson and Paul Chiodo to drive customers into the First Guardian Master Fund and the Shield Master Fund and is under ASIC investigation for allegedly receiving illegal commissions.

He was contacted for comment but did not respond. He has previously publicly denied any wrongdoing.

Mr Mackay says that, while the Federal Court proceedings have become matters of public record, they were “merely allegations made by ASIC of concerns of a particular ASIC officer held at a particular point in time, in the context of what is an ongoing and complex investigation by ASIC. They are no more”.

Shield’s Paul Chiodo is being investigated by the regulator over loans to a wholesale property fund into which ASIC alleges a large proportion (more than 50 per cent, if marketing commissions are included) of Shield’s funds had been invested.

And which had, in turn, made loans to various companies associated with Mr Chiodo to fund luxury property development projects in Fiji, Italy, Port Douglas, and Melbourne.

Mr Chiodo says these were disclosed in the fund documents.

Mr Chiodo told ABC News he had been cooperating with ASIC since 2020 when he had blown the whistle on the practices of Funds United, UGC and Seed Capital, who worked for First Guardian Capital and David Anderson.

He says people associated with the businesses he complained about had been banned by ASIC.

Mr Chiodo says he was engaged with ASIC in examinations and discussions and had recently made a complaint to ASIC regarding a fraud committed against his company.

“I am regularly engaged with ASIC in examinations and discussions regarding Keystone and Shield, and I am not aware of any allegations made by the regulator against me or my companies,” Mr Chiodo says.

Interprac denies ‘conflicted renumeration’

ASIC has also gone after the licensees that were supposed to govern the financial planners giving the advice, cancelling the licenses of MWL Financial Services, United Global Capital and Financial Services Group Australia.

The other licensee involved, Interprac is operated by ASX-listed Sequoia.

It’s the only licensee involved with Shield and First Guardian that as yet has not faced a ban.

Its CEO Garry Crole sat down for an extended interview with ABC News and says they are not worried they are next on ASIC’s hit list.

“No, I don’t [worry]. I think the licensees that they’re talking about took conflicted remuneration. We didn’t receive any conflicted remuneration.

“In fact, we took steps to stop it. We took steps to tell ASIC. ASIC were told in 2021 and did not tell us.”

Mr Crole says Interprac have since put in place a new governance committee that oversees its approved product list.

Even so, he says, “If someone commits a fraud in the future, I’m very sorry, but we probably won’t pick it up”.

Mr Crole previously wrote to investors caught up in the collapses, telling them they may be able to get “remediation” from super trustees.

Whether that happens remains to be seen.

Macquarie and ASIC had been negotiating a remediation plan for the banking giant pay investors $320 million (the amount of funds allocated to Shield through its platform between 2022 and 2023).

Ms Court says ASIC’s goal is “trying to restore as many of these funds as we can to investors”.

“We are certainly thinking of exploring every option that we can in relation to whether it be super trustees, or other options as to whether and how we can get money back to these investors who, you know, in our view, have been so wronged,” she said.

Loading…Questions over superannuation platforms

Superannuation platforms, which have been around for decades, allow financial advisers to invest on behalf of their clients in options including shares, hybrids, bonds, and managed funds. They housed the investments in Shield and First Guardian, much like a supermarket houses consumer products on its shelves.

ASIC says investments were made in First Guardian by about 6,000 investors, primarily through superannuation platforms whose trustees were Diversa, Netwealth and Equity Trustees.

First Guardian investors are owed about $500 million (liquidators FTI Consulting found First Guardian received about $642 million from investors and $197 million was redeemed, leaving $446 million outstanding).

About 5,800 people invested in Shield, primarily through Macquarie and Equity Trustees. They are owed about $480 million

Last month, ASIC announced it was suing one of the platforms, Equity Trustees, for its alleged role in the loss of $160 million of retirement savings in the Shield Master Fund.

On September 4, Equity Trustees issued a statement to the ASX saying it intended to defend the legal action.

The regulator has also flagged it could take legal action against the other platforms and reportedly has been in talks with Macquarie about getting the banking and investment giant to compensate investors.

SQM Research gave First Guardian ratings of 3.5 to 3.75 stars before withdrawing the ratings.

SQM Research managing director Louis Christopher has said the ratings were assigned to the funds “over their life cycle”, but both were downgraded “when we became concerned about limited disclosure, irregularities and a lack of information from the fund managers”.

The regulator is also looking into auditors, including the well-known BDO, which signed off on Shield’s books — BDO told ABC News it did not “provide comment on client matters” — and First Guardian auditor Auditteo (which was contacted by ABC News for comment).

Gary Prince turns 62 next month and stands to lose almost $700,000 of his superannuation.

“Every minute of every day and night it haunts me,” he said.

“I thought I was within sight of what could be something of a finish line for retirement.”

He says many investors caught up in the collapses feel “totally crushed” and some are just learning of their misfortune.

“They [investors who lost retirement savings] will be the best among us — they will be the nurses, they will be the teachers, the aged care workers,” he said.

Mr Prince says he was first contacted by comparison site Empire Wealth, which put him on to financial advisers at United Global Capital (ASIC has since put the company into liquidation and sought to ban several of its directors).

UGC financial advisers set up a self-managed super fund for Mr Prince and pumped his funds into First Guardian.

“Empire Wealth Group really picked their moment very, very well because, if you remember, in mid-2020 we were fully into COVID and all that entailed in terms of financial market turmoil,” he said.

“The [growth of the] fund that I had at the time, which was an MLC, Super Key Master Fund, had slowed.

“In the context of a fund that was going backwards, a [new] fund that seemed to be progressing at 6,7, 8 per cent was quite attractive.”

He says it only later became clear that “a lot of this was cookie-cutter advice”.

“I think he [the adviser involved] probably should have been a little bit more up-front about what First Guardian was actually investing in, rather than just talking about things like Australian shares, property, cash and so on,” he adds.

Mr Prince says he was also told his investment was diversified.

He fears that, until ASIC is properly resourced and the government steps in to overhaul the system, the 12,000 people affected by the First Guardian and Shield collapses are “simply just one of a number of canaries in the coal mine”.

“If there are people that have been proven to have misappropriated and misused funds, such as not complying with a product disclosure statement … they need to get to jail,” he said.

Compensation scheme of ‘only resort’

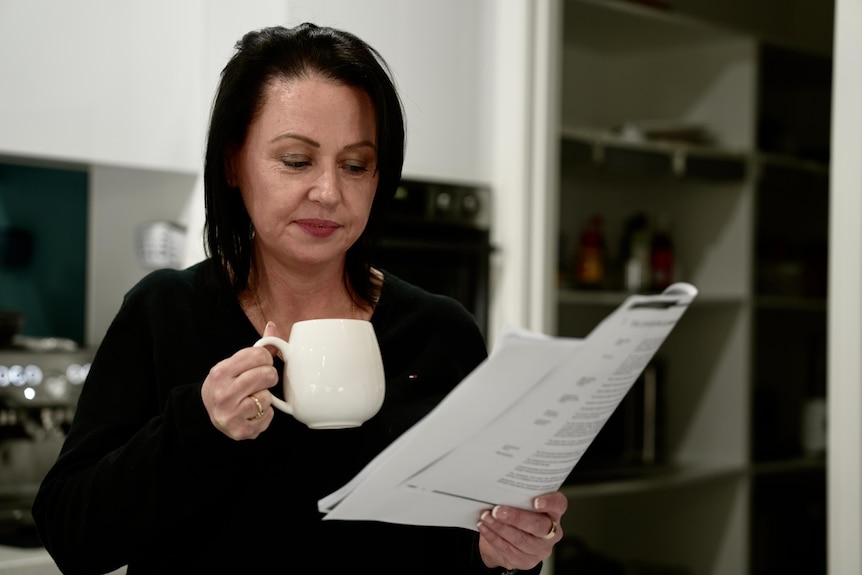

Ms Wohlers says that, before moving her retirement savings out of Hostplus and into an SMSF she had envisioned a comfortable retirement.

“I was on track to retire at 60. I had plans to travel,” she tells ABC News.

Now the money saved through her “lifetime of work” has vanished.

Ms Wohlers cannot remember what ad she clicked on, but was also first contacted by telemarketer Empire Wealth Group in late 2020, which within days connected her to a planner and signed her up.

“They were very pushy, very good salespeople and I don’t think I’d ever encountered that kind of sales tactics that they were using,” she says.

As in Mr Prince’s case, they then put Ms Wohlers onto United Global Capital.

Ms Wohlers initially had her funds invested with industry fund Hostplus, but UGC advised her to set up what she thought would be a self-managed superannuation fund.

To enable this, she was given an SOA allowing UGC’s financial advisers to move money out of her APRA-regulated Hostplus fund and channel it into First Guardian, which is not regulated by APRA.

It was promising far higher returns based on hypothetical predictions of 10-year performance.

“Straight away, the whole thing moved very quickly and, in hindsight, I can look back and go, ‘yes, it was a big decision, I should have taken more time to think about it’,” Ms Wohlers says.

By the time Ms Wohlers had cottoned on that her investments were not as diversified as she had initially been led to believe, most of her savings had been locked up.

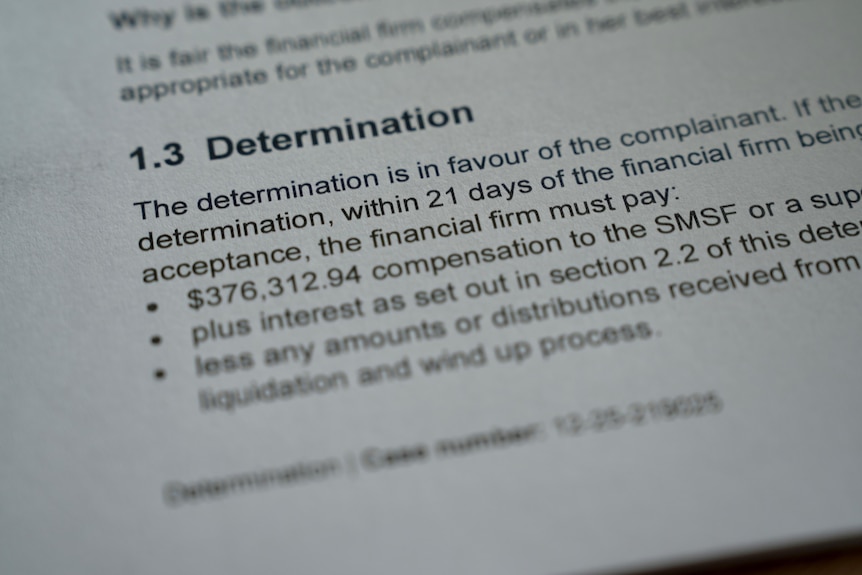

Ms Wohlers later made a complaint to the Australian Financial Complaints Authority (AFCA).

She argued she was highly pressured to make quick decisions, incorrectly told her First Guardian investment was low risk, diversified and achieved better returns than her balanced Hostplus super fund, that the advice was not specific to her individual needs or in line with her risk profile, and it was conflicted.

AFCA agreed. It found in her favour, stating that she should be awarded $376,312.94 compensation. The only problem is that, under the Compensation Scheme of Last Resort, which exists for victims of financial misconduct, individual payouts are capped at $150,000.

“I’m not looking at the compensation scheme of last resort. I’m going to suggest it’s the only resort,” Ms Wohlers said.

She hoped she could get money through the liquidation process but, as Falcon’s liquidators have noted, investors are unlikely to recover much money through that process.

Dylan Greenway is a financial adviser helping First Guardian and Shield investors lodge their cases with AFCA in the hope of recovering their money.

As he trawls through hundreds of statements of advice to investors, he has helped them identify “red flags”.

“When we’re looking at advice that’s been given, high returns are promised,” he notes.

“‘I’ve got one statement of advice that suggests the investor will receive a 15 per cent return in perpetuity on their super. It says, ‘Today you’ve got $90,000 in super. In 25 years, that will be worth $1.6 million’.

“The other issue is they [financial advisers] were putting all the investors funds in one asset, into the one fund. You don’t put all your eggs in one basket. It’s a very true thing and we’re experiencing the loss because of that.”

He says there are also issues with how people were lured in.

Mr Greenway says many of the investors were not encouraged to read their SOA and were rushed through the process.

“They’d be called by a telemarketer, who said, ‘We’ll do a comparison of your super for you’, but it was only compared with one thing, and that would be the First Guardian investment or the Shield investment,” he says.

“And then they went through a process that was quite rushed. It was transactional. Financial planning isn’t transactional; it’s a personal service. And often these people would never speak to the advisor.”

The SOA would be emailed to the investor to be docu-signed.

“They’d click the button to sign it and, bang, they were essentially locked into the investment from that point in.”

Mr Greenway says investors were often not sold on investing in First Guardian or Shield, but on well-known superannuation platforms.

“It was sold as, ‘You’re investing in Macquarie. You’re investing in NetWealth’. The client’s got a lot of comfort in that because, ‘Macquarie, well-known name, what could go wrong?'”

He says ASIC is now trying to determine whether conflicts of interests existed between the marketers, financial advisers and the people running the funds, and whether those were made clear to investors.

ASIC probe into financial planner Ferras Merhi

There are many financial planners tied to First Guardian and Shield that ASIC has attempted to ban from giving advice and is looking further into.

One it has set its sights on is Ferras Merhi.

According to ASIC, he placed more than 6,000 investors into First Guardian and Shield.

Mr Merhi was initially going to speak on camera to ABC News but, on legal advice, he reconsidered.

Mr Merhi’s lawyers note, while ASIC delivered a concise statement of claim on August 29, a detailed statement of claim has not yet been filed by the regulator.

The court has given ASIC until November 15 to file it.

In that August 29 concise statement, ASIC alleges Mr Merhi used marketing companies to push potential clients to his financial advice businesses, Venture Egg and Financial Services Group Australia (FSGA) and failed to act in the best interests of clients by giving conflicted advice and providing defective statements of advice, whilst receiving millions of dollars in fees.

Mr Merhi operated FSGA under his own licence, while his Venture Egg business operated under the Interprac license.

Between 2020 and 2024, Mr Merhi and advisers working for him allegedly advised clients to invest about $296 million of their superannuation into the First Guardian Master Fund (First Guardian) and around $230 million into the Shield Master Fund (Shield).

In return, ASIC alleges Mr Merhi’s businesses received nearly $18 million in up-front advice fees and more than $19 million from entities associated with First Guardian for marketing First Guardian to clients.

ASIC will seek to allege Mr Merhi provided clients with statements of advice which contained false or misleading statements about the nature of the Shield Master Fund by implying it was operated by Macquarie.

ASIC will also seek to allege Mr Merhi falsely represented that he had no vested interest in the recommended funds when, in reality, he was involved in marketing both schemes and received tens of millions of dollars for marketing First Guardian.

Clients were led to believe they were receiving independent, tailored advice.

Instead, ASIC argues, they were allegedly channelled into pre-determined investment portfolios that were highly risky and served the financial interests of Mr Merhi and his businesses.

Mr Merhi told ABC News in a written statement: “Every allegation of unlawful conduct that ASIC has made, and any allegation it might yet make, will be strenuously defended in the court proceedings.

“Interested non-parties may apply to the court for access to the relevant documents. My substantive defence to all allegations will be set out in those court filings.”

Were compliance staff providing oversight?

Ferras Merhi was by no means the only adviser ASIC is alleging was conflicted.

Many others operating under different licenses have come under its scrutiny.

Many of them sat under a licensee called Interprac.

Interprac’s head company, ASX-listed Sequoia, run by Garry Crole, was supposed to provide oversight of those financial planners, including Mr Merhi.

Asked about Interprac’s role and whether it increased oversight when Mr Merhi alone was bringing hundreds of clients a month into Interprac, Mr Crole said: “Absolutely. We increased oversight.”

“The compliance team was complaining to me on occasions that we were spending so much time on the oversight for that particular firm, as opposed to the 230 firms that we have oversight on.”

Mr Crole says there was “regular training of all his staff, regular reviews of his statements of advice”.

He denies there was cold calling.

“You know, the press and some of the interpretation about cold calling is not correct,” he said.

“Every member that went to Ferris or Venture Egg went on to a website from a marketing company, who said: ‘Are you unhappy with your super?'”

Asked what was going through his mind when he saw hundreds of clients coming in, from which Interprac was making fees — Mr Crole says Interprac was getting roughly 5 per cent of the thousands of dollars of fees charged to each client. That, at the very minimum, means Interprac was making millions.

“What was going through my mind was that Australians are unhappy with the superannuation system,” Mr Crole responds.

“And advisors would then give them appropriate advice. I thought that was good.”

Was Mr Crole checking Mr Merhi was giving personal advice to each one of those clients?

“Ferras Merhi was talking to every single client coming in,” Mr Crole says.

In July 2023, Interprac temporarily paused inflows into First, Guardian and Shield.

“We were in discussions with ASIC in 2023,” Mr Crole explains.

“We responded to an ASIC notice in respect to the level of business coming from lead generators.

“We determined that the investments that were being held in Shield weren’t in line with the TMD [Target market determination, which describes the market for a financial product and conditions relevant to the distribution of the product to consumers] and a number of other reasons, so we made a decision not to renew that.

He says Shield’s Paul Chiodo told Interprac: “I am investing in a few properties”.

“It [Shield] looked like it wasn’t an 80-20 fund that we’d like to believe,” Mr Crole says.

“We thought 80 per cent roughly was going to Watershed, which is a highly competent manager, and then 20 per cent was going into property.”

Two months after the pause, Interprac allowed advisors to put more client money into First Guardian.

Asked why he decided to put First Guardian and Shield on their approved product list when there was no history of performance and very little research, apart from SQM, he says: “Our standard process is to use research houses.”

“We’ve got no ability personally to look at the thousands of funds that are out there on a case-by-case basis.

“A 3.75 rating for a First Guardian or a Shield for a fund with less than three years’ experience is as high as you will ever see. It’s reasonable to expect to put those types of funds on a recommended list, from our perspective.”

Interprac allowed investors to give ‘negative consent’

The other issue that has put Mr Crole under the spotlight is reports that Interprac knew Ferris Merhi was moving clients into investments without their consent.

It was allowing advisors like Mr Merhi to issue records of advice telling the investor: “If we don’t hear back in seven days, we’ll assume you’ve given consent.”

Initially, Mr Crole denies that happened.

“We did not know that. We don’t approve negative consent,” he said.

But, pushed further, he admits a “one-off basis” negative consent model was allowed by Interprac in 2024 and argues it was done in the client’s best interest.

“We [Interprac] approved negative consent on March 24 (2024) for some cases,” he said (Mr Crole tells ABC News after the interview he got the date wrong and it was in February 2024 that the negative consent model was approved).

“Shield’s closed, client’s have been given a statement of advice, their money’s going into cash,” he notes.

“It’s not appropriate for them to go into cash, so it would then be going into where they had agreed for it to go into.”

“The issue is, clients need to get their money back,” he said.

He then blames the super funds that ran the platforms.

“The trustee did that. We did not do that. So this happened in New Quantum’s case. So New Quantum did that, they did not seek our approval, we did not know about this until after the event. Recently, they decided to ask us for that, and we did it on a one-off basis.”

Mr Crole says his message to investors who feel let down by Interprac is that he was let down too.

“We invested in APRA-regulated superannuation funds, which is appropriate. They have steps and measures that we believe and trust in,” he said.

“We believed that auditors should do their job, we believed that responsible entities should do the job, we believed the trustees should do their job.

“We believed that research houses should oversee this and we trusted that.

“Maybe I shouldn’t trust anyone in the future.”

Mr Crole also argues ASIC and Macquarie erred in placing Shield into receivership and wants to see them pay compensation to investors.

Did super trustees like Macquarie fail investors?

Financial Advice Association Australia (FAAA) CEO Sarah Abood says: “Superannuation is such an important part of consumers’ financial affairs, and they have a right to believe that that’s safe.”

“There is a lot of scrutiny right now of the role of super trustees in this process,” Ms Abood said.

“Consumers believed that they were investing with the super fund and they looked at that brand and that’s the brand they thought was looking after their money.

“But the question with the super funds is, what due diligence was done on those products (First Guardian and Shield) before they went onto the platform? Was there more that those trustees could or should have done to investigate whether those products were appropriate or not?”

Super Consumers Australia’s CEO Xavier O’Halloran says superannuation platforms “have had a huge role to play”.

“They put these products on their shelves. And as a result, people have lost money,” he said.

“Talking to consumers, they just saw the names of the platforms in a lot of cases — and these are big names: Macquarie, Equity, Trustees, Diversa — they looked at those and they had faith in those brands and so they invested their money accordingly.

“But it seems the super funds didn’t do their job in protecting people from putting these poison products on their shelves.”

ASIC’s Sarah Court says that is part of what they are examining and there may be a case for investors to get compensation from the super trustees that ran the platforms.

“That [compensation from super trustees] is one of the things that we are considering,” Ms Court says.

“We are certainly exploring every option that we can in relation to whether it be super trustees, or other options, as to whether and how we can get money back to these investors who, in our view, have been so wronged.”