Global Silicon Carbide Market Size

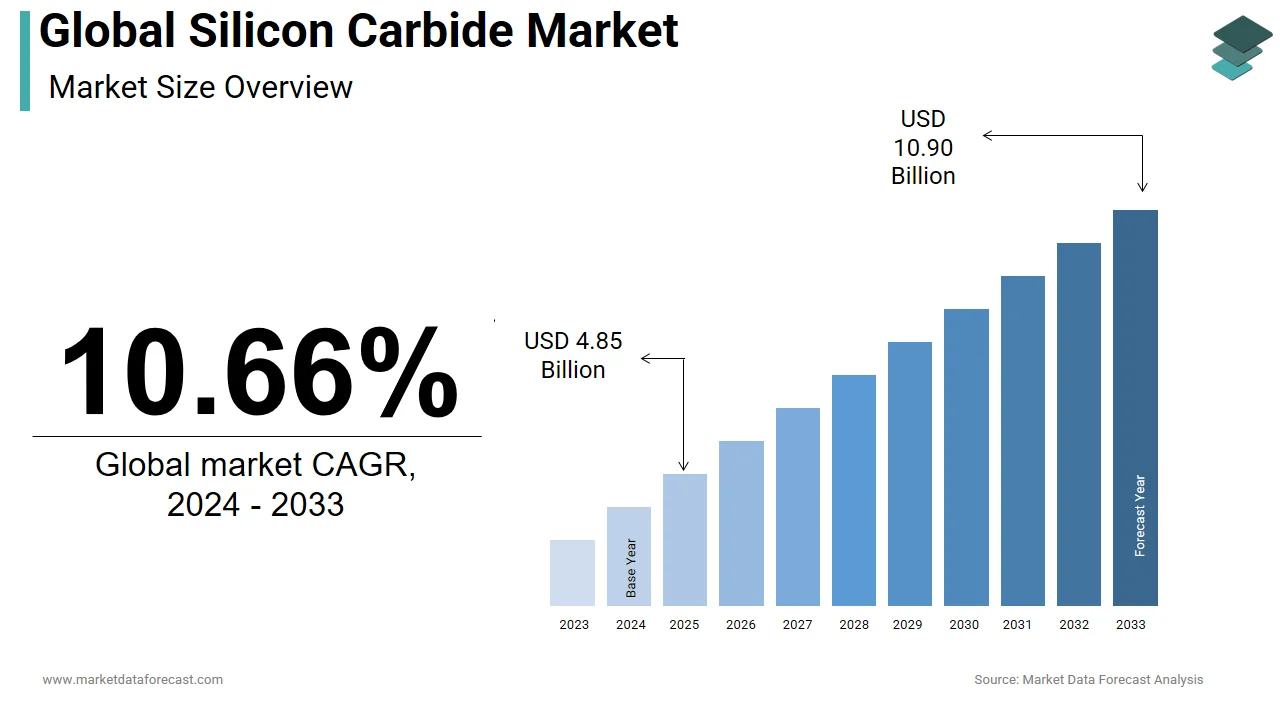

The size of the global silicon carbide market was worth USD 4.38 billion in 2024. The global market is anticipated to grow at a CAGR of 10.66% from 2025 to 2033 and be worth USD 10.90 billion by 2033 from USD 4.85 billion in 2025.

Silicon carbide is a synthetic compound of silicon and carbon, which is engineered for extreme environments where conventional semiconductors fail. Its crystalline structure enables superior thermal conductivity, electric field breakdown strength, and switching efficiency. As per data published by the U.S. Department of Energy’s Advanced Manufacturing Office, over 90% of global silicon carbide substrate production remains concentrated in fewer than ten specialized facilities, reflecting its complex manufacturing ecosystem.

MARKET DRIVERS Electrification of Premium and Performance EVs: Enhancing Power Efficiency

The electrification of automotive propulsion systems in premium and performance electric vehicles, where efficiency under load is non-negotiable, is driving the growth of the silicon carbide market. Tesla’s Model 3 Long Range, for instance, achieves a 5 to 8% efficiency gain solely from its silicon carbide inverter, as confirmed in teardown analyses by Munro & Associates. Furthermore, as per cumulative fleet data from the International Council on Clean Transportation, vehicles equipped with silicon carbide power modules demonstrate a 12% reduction in charging-induced thermal degradation over 200,000 kilometers of operation, which directly correlates to lower lifecycle ownership costs.

Integration of Silicon Carbide in Renewable Energy Systems: Enhancing Conversion Efficiency

The global transition toward renewable energy infrastructure, where silicon carbide devices enable higher-frequency switching in photovoltaic inverters and wind turbine converters, is also enhancing the growth of the silicon carbide market. According to the Fraunhofer Institute for Solar Energy Systems, utility-scale solar installations using silicon carbide MOSFETs achieve conversion efficiencies exceeding 99%, compared to 97.5% with silicon-based equivalents. This 1.5 percentage point differential translates to approximately 1.8 terawatt-hours of additional annual energy harvest per 100 gigawatts of installed global solar capacity.

MARKET RESTRAINTS Throughput Limitations and Defect Density in Bulk Crystal Growth

The persistent bulk crystal growth, where the physical vapor transport method yields substrates with throughput limitations and high defect densities, is restricting the growth of the silicon carbide market. According to peer-reviewed findings in the Journal of Crystal Growth, even state-of-the-art 200mm silicon carbide boules exhibit macrostep defect densities averaging 0.8 defects per square centimeter, rendering nearly 30% of each wafer unusable for high-reliability power devices. As per technical disclosures from Wolfspeed’s 2023 manufacturing review, the average crystal growth cycle for a single 150mm boule exceeds 14 days, compared to less than 48 hours for silicon.

Throughput Limitations and Defect Density in Bulk Crystal Growth

The prohibitive capital intensity of epitaxial deposition infrastructure, which demands ultra-high vacuum environments and precise stoichiometric control, is additionally hindering the growth of the silicon carbide market. According to equipment specifications published by Aixtron SE, a single multi-wafer silicon carbide metalorganic chemical vapor deposition reactor costs upwards of $8.5 million, nearly triple the price of comparable gallium nitride systems. As per financial disclosures from II-VI Incorporated, depreciation and maintenance of epitaxy tools account for 42% of total fabrication overhead in silicon carbide device manufacturing.

MARKET OPPORTUNITIES Expanding Adoption in Aerospace, Defense, and High-Efficiency Industrial Systems

The aerospace and defense sector, where silicon carbide’s radiation hardness and wide bandgap enable power systems for hypersonic platforms and satellite propulsion, is creating new opportunities for the growth of the silicon carbide market. According to technical assessments by the U.S. Air Force Research Laboratory, silicon carbide Schottky diodes withstand total ionizing doses exceeding 10 megarads without parametric shift, which makes them uniquely suited for orbital and near-space applications. NASA’s Glenn Research Center further confirms that silicon carbide-based DC-DC converters in deep-space probes reduce mass by 40% while doubling mean time between failures. The industrial motor drives are undergoing efficiency mandates in the European Union and China, where IE4 and IE5 classifications are becoming compulsory. According to the International Electrotechnical Commission’s 60034-30-1 standard, motors exceeding 75 kW must achieve IE4 efficiency by 2025. Silicon carbide inverters enable compliance by reducing switching losses by 60% compared to silicon IGBTs, as demonstrated in field trials by ABB across 12 mining conveyor installations.

MARKET CHALLENGES Immaturity of Back-End Packaging Technologies

The immaturity of back-end packaging technologies, where conventional wire bonding and solder materials fail under silicon carbide’s operational stress, is likely to hamper the growth of the silicon carbide market. According to reliability studies conducted by the Fraunhofer Institute for Reliability and Microintegration, aluminum wire bonds in silicon carbide modules exhibit crack propagation after 5,000 thermal cycles between -40°C and 175°C, falling short of the 15,000 cycles required for automotive qualification. As per failure analysis data from Infineon Technologies, void formation in sintered silver die-attach layers exceeds 8% after 2,000 hours of 200°C operation, triggering premature thermal runaway.

Inconsistent Performance Validation Due to Lack of Standardized Testing Protocols

The lack of standardized device characterization protocols is leading to inconsistent performance claims and design uncertainty among system integrators. According to the Power Electronics Research Group at the University of Cambridge, discrepancies in RDS(on) measurements for identical silicon carbide MOSFETs can vary by up to 22% depending on pulse width and gate drive voltage, due to incomplete industry alignment on JEDEC test conditions. As per audit findings from TÜV SÜD’s semiconductor reliability division, 37% of commercially available silicon carbide modules fail to replicate datasheet efficiency figures under real-world inductive load conditions.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2024 to 2033

Base Year

2024

Forecast Period

2025 to 2033

Segments Covered

By Product Type, Application, and Region.

Various Analyses Covered

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Regions Covered

North America, Europe, APAC, Latin America, Middle East & Africa

Market Leaders Profiled

Infineon Technologies AG, Semiconductor Components Industries, LLC (onsemi), ROHM Co., Ltd., STMicroelectronics, Wolfspeed, Inc., and others.

SEGMENTAL ANALYSIS By Product Type Insights

The black segment was the largest and held a dominant share of the global silicon carbide market in 2024, with its unmatched abrasive efficiency in metallurgical and refractory applications. The steel industry alone consumes over 1.2 million metric tons annually of black silicon carbide for deoxidation and slag conditioning, as verified by World Steel Association operational benchmarks. This mechanical superiority, coupled with raw material cost efficiencie,s black SiC is produced at nearly 40% lower energy input than green SiC, per data from the Fraunhofer Institute for Ceramic Technologies.

The green segment is lucratively growing with an expected CAGR of 18.3% during the forecast period, with its adoption in precision semiconductor wafer slicing and high-purity ceramic components for aerospace. The photovoltaic industry alone demands over 8,500 metric tons annually of green SiC abrasives to achieve sub-micron surface finishes on monocrystalline silicon wafers, according to technical specifications published by Meyer Burger Technology AG. China’s Rare Earth Industry Association confirms that over 90% of domestic dysprosium and neodymium melting operations now mandate green SiC-lined vessels to prevent metallic contamination.

By Application Insights

The steel manufacturing segment was the largest and held 44.3% of the silicon carbide market share in 2024 due to silicon carbide’s dual functionality as a potent deoxidizer and carburizer by reducing oxygen content in molten steel by up to 75% compared to ferrosilicon alone, according to metallurgical efficiency audits conducted by ArcelorMittal’s Ghent R&D facility. The material’s exothermic reaction during dissolution releases 6,800 kJ/kg of thermal energy, effectively lowering furnace energy input by 8–12%, as measured in operational trials by Nippon Steel’s Kimitsu Works.

The Automotive segment is expected to register a CAGR of 29.7% during the forecast period as every battery electric vehicle requires between 50 and 120 grams of silicon carbide die content for onboard chargers and traction inverters, depending on voltage architecture. Furthermore, as per efficiency certification data from TÜV Rheinland, SiC-based systems enable regenerative braking energy recovery rates of 89%, compared to 76% with silicon IGBTs, which directly extends driving range by 7–9% per charge cycle.

REGIONAL ANALYSIS Asia Pacific Market Analysis

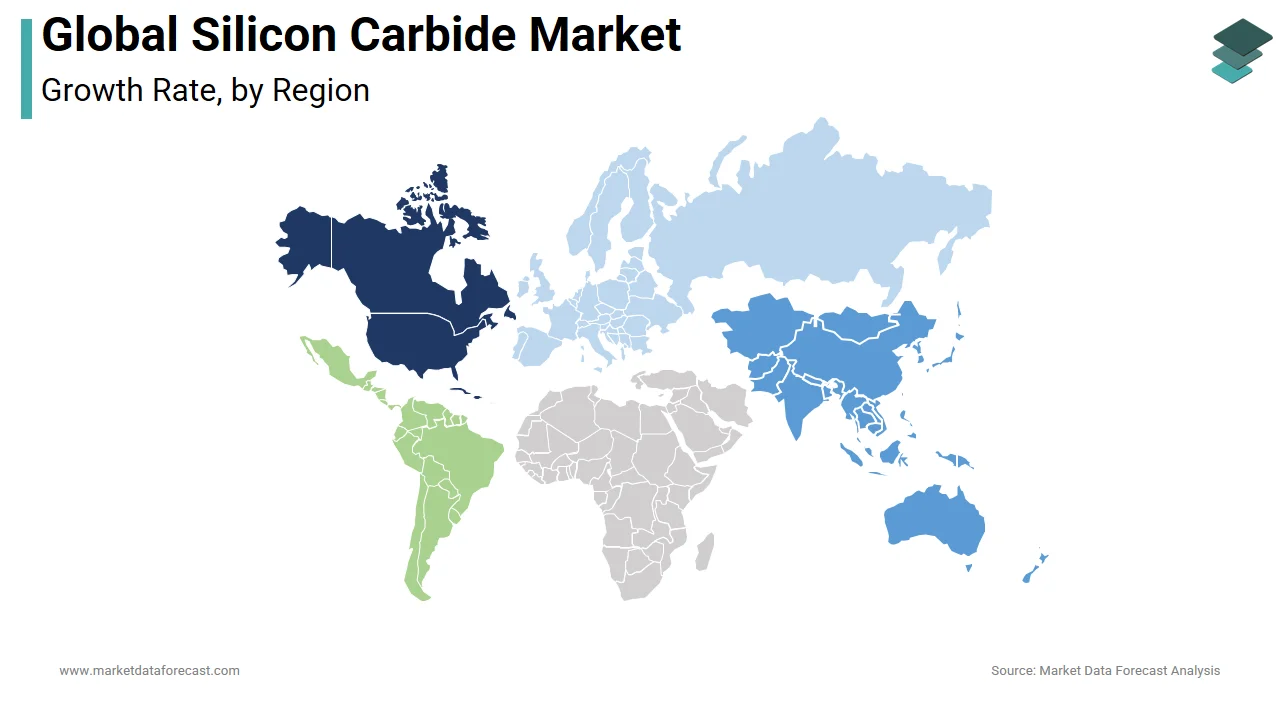

Asia Pacific played the dominating role in the global market by accounting for 37.3% of the global market share in 2024. The region’s dominance is driven by its position as the world’s epicenter for semiconductor manufacturing, electric vehicle production, and renewable energy deployment. China is the primary contributor, consuming over 45% of the region’s SiC wafers for use in EV power modules and industrial motor drives, as reported by the China Electronics Materials Association. The Chinese government has prioritized wide-bandgap semiconductors under its Five-Year Plan for Integrated Circuit Development, allocating USD 15 billion in subsidies between 2021 and 2025 to reduce import dependency. Japan and South Korea are key innovators in device fabrication, with companies like Rohm Semiconductor and Fuji Electric leading in SiC MOSFET and diode commercialization. Taiwan’s TSMC has begun integrating SiC into niche power ICs, supporting data center efficiency. Additionally, India is emerging as a downstream adopter, with Tata Motors and Mahindra incorporating SiC inverters into next-generation EVs. As per the Institute of Electrical and Electronics Engineers, SiC-based traction inverters improve EV range by up to 7%, reinforcing their strategic importance. With strong policy backing, expanding EV infrastructure, and growing investments in domestic wafer production, the Asia Pacific region remains at the forefront of SiC adoption, shaping global supply chains and technological standards.

North America Market Analysis

North America Market Analysis

North America is another market regional segment in the global market and occupied the second largest share of the worldwide market in 2024. The United States is the dominant force, home to leading material producers such as Wolfspeed, ON Semiconductor, and II-VI Incorporated, which supply high-purity SiC substrates for aerospace, defense, and automotive applications. The U.S. Department of Defense has funded multiple initiatives under the Wide Bandgap Semiconductor Technology program, investing over USD 800 million since 2020 to advance SiC-based radar and electronic warfare systems, as confirmed by the Defense Advanced Research Projects Agency. In the automotive sector, Tesla’s early adoption of SiC in Model 3 inverters set a precedent, prompting Ford, General Motors, and Lucid Motors to follow suit. According to Argonne National Laboratory, over 60% of new U.S.-based EV platforms now integrate SiC power electronics to enhance efficiency and reduce battery load. Federal incentives under the CHIPS and Science Act have accelerated domestic wafer capacity expansion, with Wolfspeed commissioning a USD 1.3 billion fab in North Carolina, the largest dedicated SiC facility globally. Canada supports the ecosystem through research at institutions like McMaster University, focusing on grid-scale power conversion. With deep technological expertise, robust venture funding, and strong public-private collaboration, North America maintains leadership in innovation and high-performance application development.

Europe Market Analysis

Europe is likely to account for a prominent share of the global market over the forecast period, owing to its aggressive decarbonization agenda and advanced automotive engineering base. Germany, France, and Sweden are central to demand, where automakers such as BMW, Volkswagen, and Volvo are integrating SiC into EV inverters to meet stringent CO₂ emission targets. As per the European Automobile Manufacturers Association, over 80% of premium EV models launched in Europe in 2023 featured SiC-based power systems, improving charging speed and driving efficiency. Infineon Technologies, headquartered in Germany, is one of the largest SiC device manufacturers in the world, operating 150mm and transitioning to 200mm wafer lines to scale production. STMicroelectronics in France and Italy has secured long-term supply agreements with Renault and Geely to support European EV electrification. Additionally, the EU’s Green Deal and REPowerEU plans are accelerating renewable energy integration, increasing demand for SiC in solar inverters and grid infrastructure. A report by Fraunhofer ISE found that SiC-enabled photovoltaic inverters achieve 99% efficiency, reducing energy loss by 30% compared to silicon-based systems. With harmonized regulatory frameworks, strong industrial policy, and investment in local semiconductor sovereignty, Europe is positioning itself as a self-reliant hub for sustainable SiC technology deployment.

Latin America Market Analysis

Latin America is predicted to register steady growth in the global market during the forecast period. Brazil leads the region in demand, primarily driven by industrial automation, mining operations, and the modernization of power transmission networks. The Brazilian Ministry of Mines and Energy has initiated grid upgrade projects incorporating SiC-based converters to minimize losses in long-distance electricity distribution, particularly in remote Amazonian regions. Chile’s rapidly expanding solar power sector, now exceeding 5 gigawatts of installed capacity as reported by the Chilean Energy Minister, is beginning to adopt SiC inverters to maximize output from high-altitude installations. Argentina has seen pilot deployments of SiC modules in rail traction systems to improve energy efficiency in urban transit. However, high upfront costs and limited local technical expertise remain barriers to widespread implementation. As per the Inter-American Development Bank, less than 10% of industrial motor drives in the region use advanced power semiconductors, indicating significant untapped potential. Multinational suppliers such as ABB and Siemens are supporting knowledge transfer through training programs for engineers. While current consumption is low, rising investment in smart grids, EV infrastructure, and renewable integration suggests that Latin America could become a meaningful secondary market for SiC in the coming decade, particularly as global supply diversifies and pricing becomes more accessible.

Middle East and Africa Market Analysis

The market in the Middle East and Africa is projected to witness a moderate CAGR during the forecast period. Demand is concentrated in the Gulf Cooperation Council (GCC) countries, where national visions such as Saudi Arabia’s Vision 2030 and the UAE’s Net Zero 2050 strategy are driving investments in smart grids, desalination plants, and renewable energy infrastructure all areas where SiC enhances efficiency. In the UAE, Masdar City and Dubai Electricity and Water Authority have deployed SiC-based inverters in solar farms, achieving a 4% improvement in energy yield, as reported by the International Renewable Energy Agency. Saudi Arabia’s NEOM megaproject includes plans for fully electrified transport and green hydrogen production, both reliant on high-efficiency power electronics. South Africa is the primary market in Sub-Saharan Africa, using SiC modules in mining conveyor systems and rail networks to reduce downtime and energy consumption. However, broader adoption is constrained by limited semiconductor manufacturing capabilities and reliance on imported components. According to the World Bank, only two countries in the region have active semiconductor research labs. Despite these challenges, partnerships with European and Asian technology providers are enabling knowledge transfer. With increasing focus on reducing carbon intensity and modernizing aging infrastructure, the region is laying the groundwork for future SiC integration, particularly in energy-intensive sectors critical to economic diversification.

COMPETITIVE LANDSCAPE

The silicon carbide market is marked by fierce competition as global leaders race to dominate the Asia Pacific’s EV and renewable energy sectors. Differentiation stems from application-specific innovation, localized manufacturing, and deep customer collaboration rather than pricing. Strategic alliances with governments and supply chain partners help navigate regulations and secure raw materials. Rapid advancements in device performance, packaging, and thermal management define the innovation curve.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global silicon carbide market include

- Infineon Technologies AG

- Semiconductor Components Industries, LLC (onsemi)

- ROHM Co., Ltd.

- STMicroelectronics

- Wolfspeed, Inc.

Top Strategies Used by the Key Market Participants

Key players deploy vertical integration to secure substrate quality and supply continuity. They form strategic partnerships with regional manufacturers to enable localized production and reduce geopolitical risk. Heavy R&D investments focus on application-specific device optimization for EVs, solar, and industrial systems. Companies expand technical support teams across Asia Pacific nations to assist OEMs during design cycles.

Top Players in the Silicon Carbide Market

- Wolfspeed is accelerating its global footprint with advanced manufacturing and deep regional integration in the Asia Pacific. In April 2024, it inaugurated a 200mm SiC fab in Germany to enhance global supply resilience while reducing delivery times to Asian customers. The company established R&D centers in Japan and South Korea to co-develop application-specific devices for EV fast-charging and industrial systems. Multi-year supply agreements with leading Asian EV makers ensure technology alignment. These moves reinforce Wolfspeed’s role as a strategic innovation partner, enabling faster adoption of SiC solutions across high-growth power electronics markets in the region.

- STMicroelectronics is strengthening its Asia Pacific presence through localized production and customer-centric innovation. In June 2023, it partnered with China’s Sanan IC to co-manufacture 8-inch SiC wafers, reducing logistics lead times and enhancing supply stability. The company launched new SiC MOSFET families optimized for regional solar and EV inverter designs. Field application teams were expanded across India, Taiwan, and Thailand to provide real-time design support.

- Infineon is leveraging portfolio expansion and regional infrastructure to enhance its SiC position in the Asia Pacific. Its September 2023 acquisition of GaN Systems enhances system-level design capabilities applicable to SiC modules in EVs and renewables. The company launched CoolSiC™ automotive MOSFETs tailored for Japanese and Korean platforms and upgraded logistics hubs in Singapore and Malaysia for just-in-time delivery. Collaborative design labs in Shanghai and Bangalore accelerate co-innovation with local customers. These actions deepen Infineon’s integration into regional supply chains and position it as a holistic solution provider, enabling faster time-to-market and greater design flexibility for Asia’s evolving power electronics landscape.

GLOBAL SILICON CARBIDE MARKET NEWS

- In June 2023, STMicroelectronics, a global semiconductor innovator, partnered with Sanan IC to co-manufacture 8-inch silicon carbide wafers in China. This silicon carbide market collaboration enables localized production, reducing lead times and logistics costs for Asia Pacific clients. STMicroelectronics concurrently introduced new SiC MOSFET families optimized for regional solar and EV inverter designs. Expanded field engineering teams in India and Thailand provide real-time design support. These initiatives reinforce ST’s position as a responsive, innovation-centric partner deeply embedded in Asia Pacific’s next-generation power conversion and mobility silicon carbide market ecosystems.

MARKET SEGMENTATION

This research report on the global silicon carbide market has been segmented and sub-segmented into the following categories.

By Product Type

- Black Silicon Carbide

- Green Silicon Carbide

- Other Products (Metallurgical-grade SiC, etc.)

By Application

- Steel Manufacturing

- Energy

- Automotive

- Aerospace and Defense

- Electronics and Semiconductors

- Other Applications (Industrial Manufacturing, Abrasives and Ceramics, etc.)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa