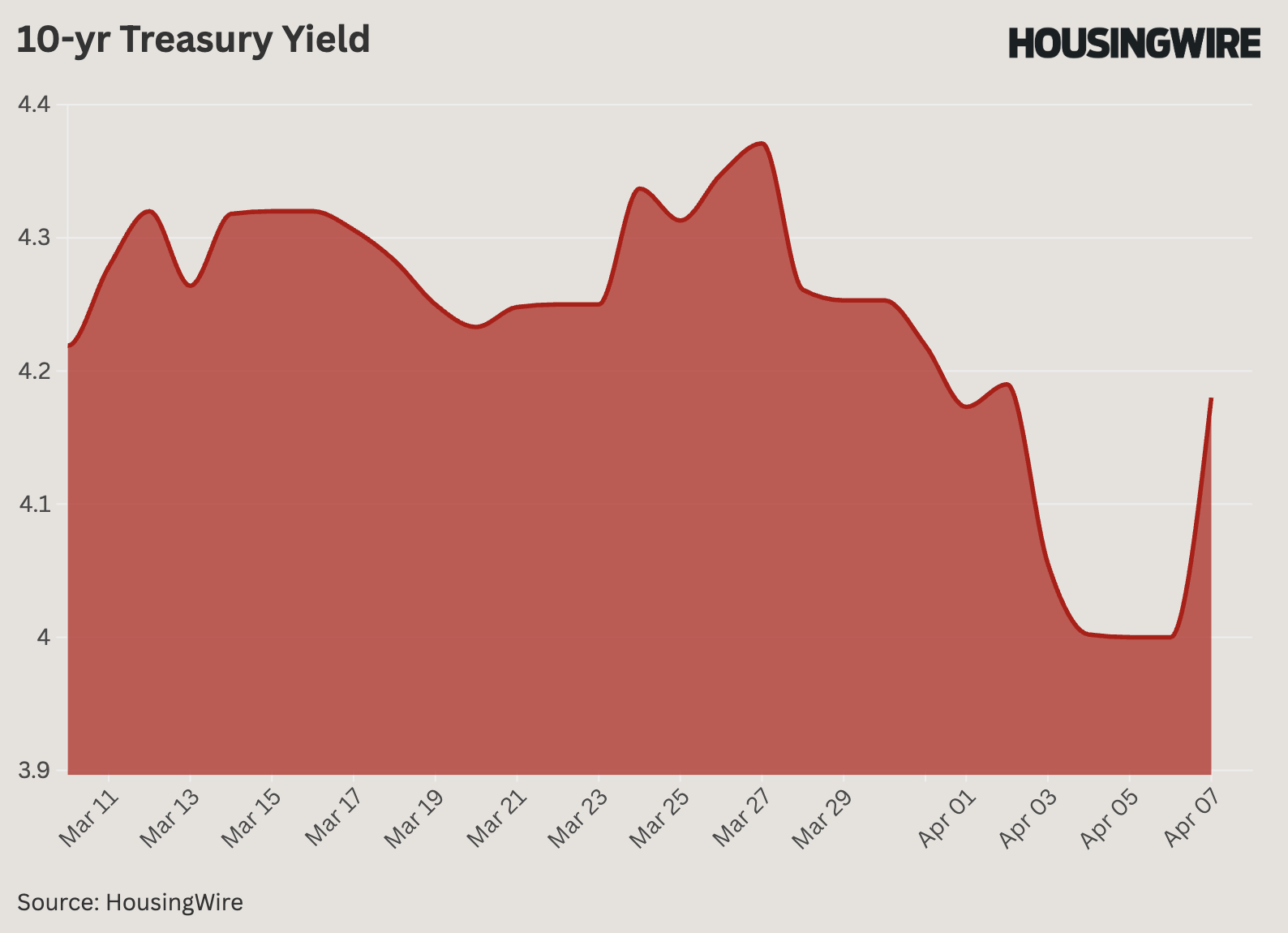

Here is a visual of the 10-year yield over the past few days

On Friday morning, one of my early tweets on X was that the 10-year yield would be at 4.35% — if it weren’t for the Godzilla tariffs. That’s because the labor data didn’t warrant the bond market buying. Stocks were selling off like crazy, and money flowed into the bond market so fast that we almost got close to my low-end forecast of 3.80%. I had a forecast range of the 10-year yield between 4.70% and 3.80%. For the most part, we have stayed in that range. However, we got as low as 3.87% recently due to market volatility.

Over the past few days, the market’s volatile reaction to headlines has been so extreme that we are due for a significant reversal if any positive news on trade deals emerges. We are witnessing that today, with stocks and the bond market showing movement over the last two days.

If the labor market data had been disappointing, it would justify lower yields, similar to what we experienced last year. However, that has not been the case so far. We have seen a series of economic data points weaken, which has resulted in lower 10-year yields and mortgage rates from their peak. However, last week’s labor data was acceptable. Still, anything below 4.35% on the 10-year yield can be warranted on future economic concerns, but the move down toward 3.87% was too much. Of course, with market volatility, mortgage spreads do get worse.

We understand that the current situation can feel overwhelming. As time passes, it will improve. The softening in economic data we’ve experienced this year suggests that a 10-year yield of 4.35% or lower is reasonable. However, the recent decline was driven mainly by an unprepared global marketplace facing unexpected tariffs, resulting in significant market turmoil. The reversal in yields and rates is the result of that, too.