Europe Liver Disease Therapeutic Market Outlook

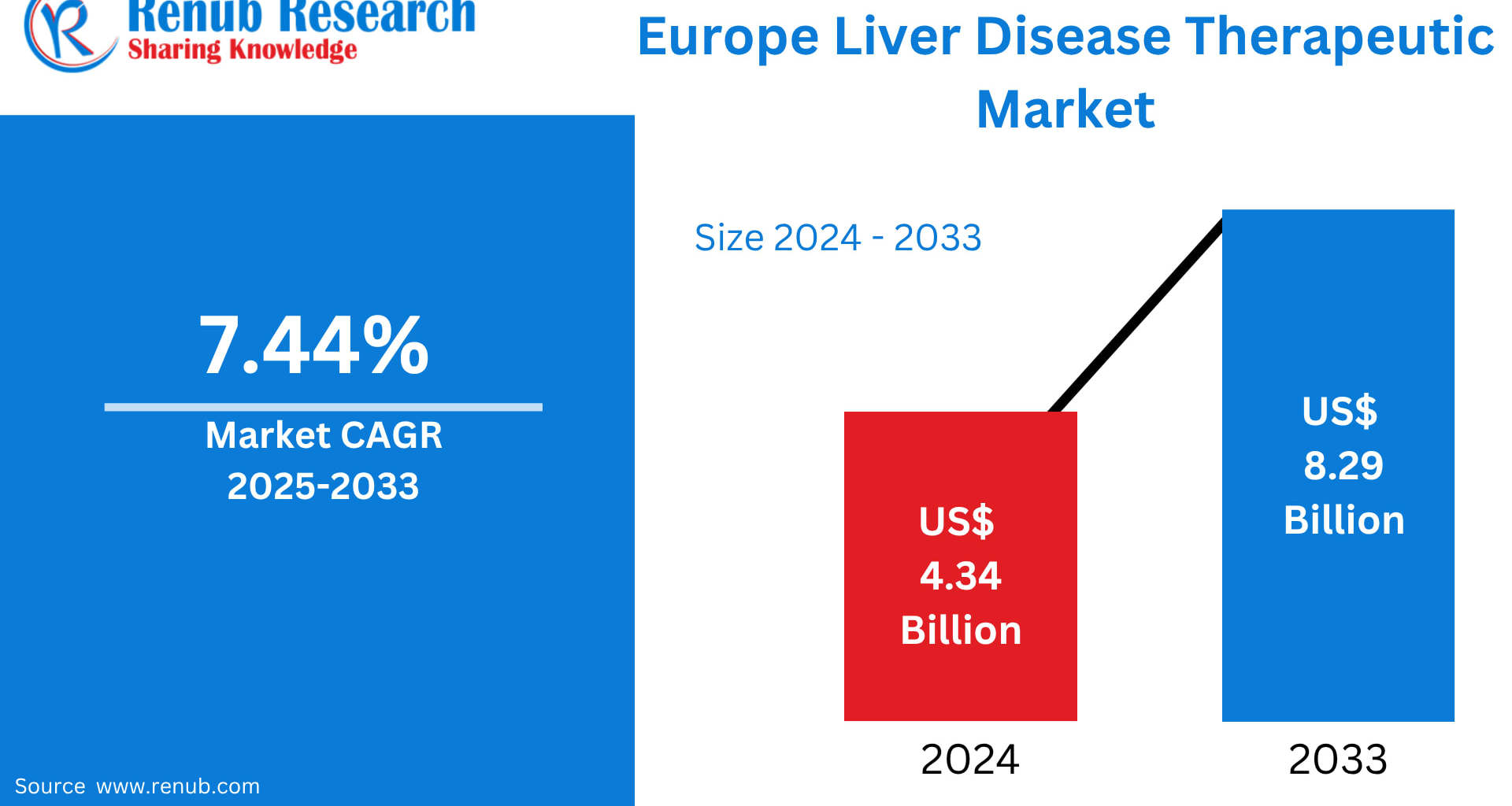

The Europe Liver Disease Therapeutic Market is projected to grow from US$ 4.34 billion in 2024 to US$ 8.29 billion by 2033, registering a CAGR of 7.44% from 2025 to 2033, according to Renub Research estimates. This impressive growth trajectory reflects the rising prevalence of liver-related disorders, rapid advancements in pharmaceutical and biologic therapies, and heightened awareness around early diagnosis and disease management across European healthcare systems.

Across Europe, lifestyle changes, aging populations, obesity, alcohol consumption, and persistent viral infections such as Hepatitis B and C continue to elevate the clinical and economic burden of liver diseases. In response, governments, healthcare providers, and pharmaceutical companies are intensifying investments in screening programs, clinical trials, and next-generation therapeutics—cementing liver disease treatment as a critical pillar of Europe’s healthcare ecosystem.

Key Growth Drivers in the Europe Liver Disease Therapeutic Market

Increasing Incidence of Liver Diseases

Europe faces a substantial and growing liver disease burden. Liver cirrhosis alone accounts for nearly 170,000 deaths annually across the continent. The rising prevalence of NAFLD—closely linked to obesity, sedentary lifestyles, and metabolic disorders—has emerged as one of the most significant contributors to market growth.

Alcohol consumption patterns in several European countries further exacerbate the incidence of alcoholic liver disease, while viral hepatitis remains a persistent public health challenge despite vaccination and awareness programs. This confluence of factors has led to increased hospital admissions, long-term treatment requirements, and higher demand for effective therapeutic interventions, directly fueling market expansion.

Advancements in Therapeutic Solutions

Scientific innovation is transforming liver disease management in Europe. Breakthroughs in antiviral drugs, biologics, immunotherapies, and antifibrotic agents are significantly improving patient outcomes. The growing focus on regenerative medicine, including stem cell–based approaches and RNA-targeted therapies, is opening new frontiers for treating liver fibrosis and metabolic-associated steatotic hepatitis (MASH).

A notable milestone occurred in October 2024, when the European Commission granted conditional approval to Iqirvo (elafibranor) 80 mg tablets for the treatment of primary biliary cholangitis (PBC) in combination with ursodeoxycholic acid (UDCA). This approval underscores Europe’s commitment to accelerating access to innovative therapies for rare and complex liver conditions.

Supportive Government and Research Initiatives

European governments are actively prioritizing liver health through comprehensive public health programs aimed at reducing mortality and long-term complications. These initiatives emphasize early diagnosis, lifestyle interventions, vaccination, and timely therapeutic management.

In February 2024, a pioneering research initiative at Hanover Medical School (MHH) launched an ambitious project exploring RNA-based therapies for liver fibrosis and MASH. Backed by approximately £500,000 in funding from the Boehringer Ingelheim Foundation under its Rise Up! program, the project highlights the growing role of cutting-edge biomedical research in shaping the future of liver disease therapeutics in Europe.

Challenges Facing the Europe Liver Disease Therapeutic Market

High Cost of Advanced Treatments

Despite therapeutic progress, the high cost of advanced liver disease treatments remains a major barrier. Antiviral regimens, immunotherapies, targeted oncology drugs, and liver transplantation procedures impose significant financial strain on healthcare systems. In countries with constrained healthcare budgets or limited reimbursement frameworks, patient access to these life-saving therapies may be restricted, potentially slowing market growth.

Limited Awareness and Late Diagnosis

Many liver diseases progress silently, exhibiting minimal symptoms until advanced stages. Late diagnosis reduces treatment efficacy and increases healthcare costs. Although awareness campaigns have improved screening rates, early detection remains suboptimal in several European regions. This challenge continues to limit the full potential of therapeutic interventions and underscores the need for sustained public education and routine screening initiatives.

Market Segmentation Insights

Europe Liver Disease Chemotherapy Drugs Market

Chemotherapy drugs play a critical role in treating hepatocellular carcinoma (HCC), the most common form of liver cancer. When surgical intervention is not feasible, chemotherapy and targeted oncology therapies offer viable treatment pathways. Ongoing research to improve drug safety and efficacy is enhancing survival outcomes and driving demand across Europe’s oncology care settings.

Europe Liver Disease Therapeutic Vaccines Market

Therapeutic vaccines targeting viral hepatitis represent a rapidly evolving segment. These vaccines aim to stimulate immune responses capable of controlling or eliminating chronic infections such as Hepatitis B and C. Increased R&D investments and government-backed vaccination programs are supporting steady growth in this segment.

Europe Liver Disease Therapeutic Viral Hepatitis Market

Viral hepatitis remains a dominant contributor to liver disease prevalence in Europe. Expanded screening programs, improved access to antiviral therapies, and robust public health campaigns are accelerating treatment uptake. Pharmaceutical innovation continues to strengthen this segment’s growth prospects.

Europe Alcoholic Liver Disease Market

Alcoholic liver disease persists as a major public health issue due to cultural and social drinking patterns. Demand for pharmacological treatments, behavioral interventions, and transplant services continues to rise. Government initiatives focused on alcohol consumption reduction and early intervention are contributing to sustained market growth.

Europe Liver Disease Therapeutic Hospitals Market

Hospitals serve as the primary treatment hubs for liver disease patients, offering diagnostic services, specialized care, and advanced therapeutic options. Investments in modern infrastructure, skilled hepatologists, and multidisciplinary care models are driving growth in this end-user segment.

Country-Level Market Highlights

France

France benefits from a robust healthcare system and proactive liver health policies. Strong emphasis on hepatitis screening, cirrhosis management, and early diagnosis makes France a key contributor to the European market.

United Kingdom

The UK market is expanding due to rising NAFLD and alcoholic liver disease cases. National Health Service (NHS) initiatives, combined with pharmaceutical innovation and public awareness campaigns, support consistent growth.

Netherlands

Advanced healthcare infrastructure and effective public health strategies underpin steady market expansion in the Netherlands, particularly in hepatitis management and early disease detection.

Russia

Russia faces a high incidence of viral hepatitis and lifestyle-related liver disorders. While rural healthcare access remains a challenge, government investments and urban healthcare development are driving increased demand for advanced therapeutics.

Market Segmentation Overview

By Therapy Type

Anti-Rejection Drugs / Immunosuppressants

Chemotherapy Drugs

Targeted Therapy

Vaccines

Immunoglobulins

Corticosteroids

Anti-Viral Drugs

By Disease Type

Non-alcoholic Fatty Liver Disease (NAFLD)

Viral Hepatitis (B, C, D)

Alcoholic Liver Disease (ALD)

Autoimmune Liver Disease

By End Users

Hospitals

Laboratories

Others

By Country

France, Germany, Italy, Spain, United Kingdom

Belgium, Netherlands, Russia, Poland

Greece, Norway, Romania, Portugal

Rest of Europe

Competitive Landscape and Key Players

The Europe liver disease therapeutic market is highly competitive, with leading pharmaceutical companies focusing on innovation, clinical trials, and strategic collaborations. Key players analyzed across five viewpoints—overview, key personnel, recent developments, SWOT analysis, and revenue performance—include:

Abbott Laboratories

Astellas Pharma Inc.

Bristol-Myers Squibb

Gilead Sciences

GlaxoSmithKline Pharmaceuticals Ltd

F. Hoffmann-La Roche Ltd

Merck & Co. Inc.

Novartis AG

Sanofi S.A

Pfizer Inc.

Takeda Pharmaceuticals

Final Thoughts

The Europe Liver Disease Therapeutic Market is entering a dynamic growth phase driven by rising disease prevalence, strong government support, and rapid therapeutic innovation. While challenges such as high treatment costs and late diagnosis persist, continued investments in research, public health initiatives, and next-generation therapies are expected to significantly improve patient outcomes.

As Europe strengthens its commitment to liver health through innovation and policy support, the market is well-positioned to deliver sustainable growth and transformative healthcare solutions through 2033 and beyond.