This report is from this week’s CNBC’s UK Exchange newsletter. Like what you see? You can subscribe here.

The dispatch

A new year brings with it optimism for the coming 12 months

The main hope for the U.K. must be that 2026 proves to be better — for the economy, households and individual businesses — than 2025.

People visit a lookout point in Greenwich Park, with the Canary Wharf financial district in the distance, during sunny weather but cold weather in London, U.K., on Jan. 2, 2026.

Henry Nicholls | Afp | Getty Images

The economy entered the new year flatlining and, while in 2025 the FTSE 100 index enjoyed its best one-year gain since 2009, that was hardly indicative of the health of many individual businesses.

With that in mind, here are five things to watch for the year ahead:

Rate cuts

The first is how much the Bank of England presses ahead with further interest rate cuts. It cut the Bank Rate four times during 2025, fewer times than expected, taking its main policy rate from 4.75% to 3.75%. Markets expect further reductions during 2026, but not to the extent that was being anticipated this time last year.

The rate-setting Monetary Policy Committee made clear at its last meeting, on Dec. 18, that interest rates were still on a downward path, but noted that, with every cut, this would become a closer call. Four of the nine-member committee voted against December’s rate cut and clearly worry that, with inflation at 3.2%, appreciably higher than the Bank’s target rate of 2%, the scope for going further is limited.

Of particular concern is that, as committee hawk Catherine Mann put it last month, “elevated household inflation expectations … have formed during a prolonged high‑inflation environment.”

That was borne out by the Bank’s latest quarterly Inflation Attitudes Survey published last month, revealing that median expectations for inflation over the coming year were 3.5%, although this was down from 3.6% previously.

On that basis, while further rate reductions are expected during 2026, it would be unwise to bet on the terminal rate — the level at which rate cuts end — falling below 3%.

If it does, that will be because of concerns over unemployment — the second thing to watch for.

Unemployment jitters

The jobless rate in the U.K. at the end of October — the latest month for which figures are available — stood at 5.1%, its highest since March 2021, when the economy was emerging from the last of the three Covid lockdowns.

Job vacancies have fallen steadily since peaking in mid-2022 and, at the end of November, stood at 729,000 — around the level they have been since May. Much of the blame for this is targeted at Rachel Reeves, the chancellor of the Exchequer (U.K. finance minister), who raised payroll taxes in her first Budget in October 2024 and added to the cost of hiring people in her most recent fiscal event last November.

With productivity stagnant, the jobless rate is expected to rise in 2026.

The Resolution Foundation, a left-of-center think tank enjoying close ties with the government, warned this week that a combination of the higher minimum wage, elevated energy prices and a prolonged period of higher interest rates could finally kill the thousands of so-called “zombie firms” — those firms able to service their debts but do little else — that somehow stayed afloat between 2009 and 2022 when interest rates were close to zero.

A jobless rate of 5.5% would represent an 11-year high, signaling trouble for Reeves, the third thing to watch for.

Chancellor challenges

The bookmakers, who tend to get these things right, expect her to leave office this year with William Hill putting the odds of her exit at 4/9. That said, Reeves was priced at very short odds to step down last year, only to survive.

Top-touted possible replacements include Work and Pensions Secretary Pat McFadden, a wily operator and one of the few ministers who served in the last Labour government, while second favourite is Torsten Bell, a junior Treasury minister and former head of the Resolution Foundation, although he could face competition from the youthful Darren Jones. The latter’s strong performance as chief secretary to the Treasury recently persuaded Prime Minister Keir Starmer to give him a newly created role — chief secretary to the PM — in the heart of government.

Business confidence

The fourth thing to watch for will be whether U.K. business regains its mojo. Business investment in the U.K. was again the weakest in the G7 group of economies in 2025 and was negative in two of the last four quarters although recent survey data indicates it should have turned positive in the final three months of the year.

However, 2025 marked an improvement on 2024 and would probably have been better still had it not been for the volatility caused by U.S. President Donald Trump’s tariffs, which severely hit confidence. Expectations are for investment to continue recovering in 2026, but it is likely to be concentrated in areas like research and development and intellectual property rather than in tangibles such as buildings and equipment.

The ranks of big business will also be worth watching as a number of new chief executives take the helm at FTSE 100 heavyweights including BP, Diageo, GSK and Severn Trent.

Going public

The final thing to watch for is whether, at long last, IPOs recover to traditional levels. There were just 22 IPOs in London in 2025 — up from a mere 16 in 2024 — and well below the historic average.

However, bankers hope investors have regained their appetite to invest in new issues following the market’s solid performance last year, along with recent reforms and regulatory changes aimed at making London a more attractive destination in which to list.

All eyes are on Visma, a Norwegian software group backed by the private equity firm Hg Capital, which recently chose to list in London over Amsterdam. In 2023, it was valued at 19 billion euros ($16.45 billion) in a private share sale.

Others which could come to market this year include the challenger banks Monzo and Starling, the credit-checking firm ClearScore and even Howden, the insurance broking giant famous for its sponsorship of the British and Irish Lions rugby team.

With Reeves having launched a three-year stamp duty holiday for new listings in her November Budget, hopes are high that at least some of these names will come to market and attract a decent following.

Of course, there’s one final factor that could be a huge boost to sentiment: the football (or soccer…) World Cup, hosted by Canada, the U.S. and Mexico, which kicks off on June 11. Should England emerge victorious for the first time in 60 years, it would be of unimaginable value to the economy. Don’t hold your breath, though.

Top TV picks on CNBC

Dan Mahoney, senior U.K. economist at Handelsbanken, discusses U.K. Prime Minister Keir Starmer’s policy to seek closer alignment with the EU Single Market.

Ritika Gupta looks back at a year dominated by Budget turbulence for the U.K.’s Labour Party government, and what could be ahead in 2026.

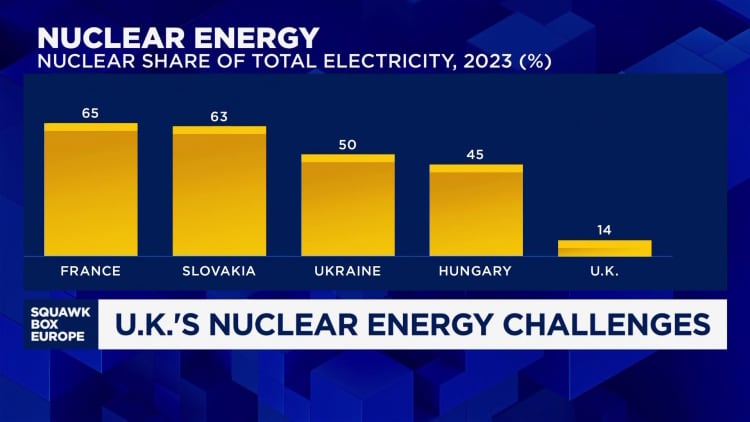

The U.K. was the birthplace of commercial nuclear energy, but now generates just a fraction of its power from it. Tasmin Lockwood has been looking at how the country’s government is looking to unlock a “golden age of nuclear.”

Need to know

UK’s Octopus Energy to spinoff AI unit Kraken. Origin Energy, which holds a major stake in Octopus, said in a statement late on Monday that Octopus had raised $1 billion in its first standalone funding round, valuing the business at $8.65 billion.

Has the UK’s AI infrastructure buildout been a success? The U.K. announced its AI Opportunities Action Plan in January last year. But critics point to energy restrictions and slow buildouts as signs the country is at risk of lagging further global rivals in the AI race.

UK stocks outperformed Wall Street in 2025. London’s benchmark FTSE 100 index gained more than 21% last year, ahead of the S&P 500‘s 16.39% rise. Analysts think the FTSE 100 could advance even further in 2026.

— Holly Ellyatt

Quote of the week

I think the British Prime Minister has a particularly good relationship with Donald Trump, and that’s to our advantage as a country … it’s to Britain’s disadvantage if we end up with international law breaking down.

— Emily Thornberry, chair of the U.K. Foreign Affairs Select Committee

In the markets

The FTSE 100 made history this past week, breaking through the landmark 10,000 level on the opening trading day of 2026 for the first time since launching in January 1984. The U.K.’s blue-chip index gained 1.2% on Tuesday, finishing the session at 10,122.73, up from 9,931.38 a week ago.

The British pound, meanwhile, has made a positive start to the year against the dollar. Sterling stood at $1.3493 on Tuesday afternoon London time, advancing from $1.3473 against the greenback last Wednesday.

Yields on the U.K. government’s benchmark 10-year bonds — also known as gilts — also edged higher, ending Tuesday at 4.487% compared to 4.474% a week ago.

Stock Chart IconStock chart icon

The performance of the Financial Times Stock Exchange 100 Index over the past year.

— Hugh Leask

Coming up

Jan. 8: Halifax House Price Index for December

Jan. 13: BRC retail sales for December

Jan. 15: U.K. GDP data for November