Industrial Vacuum Cleaner Market Overview

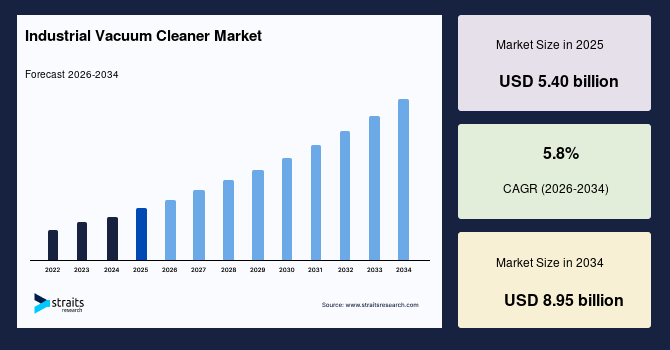

The global industrial vacuum cleaner market size was estimated at USD 5.40 billion in 2025 and is anticipated to grow from USD 5.72 billion in 2026 till USD 8.95 billion by 2034, growing at a CAGR of 5.8% from 2026-2034. The surge in the global market can be attributed to reinforced workplace safety and environmental policies, the proliferation of industrial automation, including cobots and AMRs that rely on integrated cleaning solutions, and the rising need for contamination prevention in industries like semiconductors, pharmaceuticals, and additive manufacturing.

Key Market Trends & Insights

- Europe held a dominant share of the global market with a market share of 35% in 2025.

- The Asia Pacific region is growing at the fastest pace, with a CAGR of 7.9%.

- Based on product type, the portable or handheld industrial vacuums are estimated to grow at a CAGR of 10.4%.

- Based on end-use industry, manufacturing led, holding a market share of 28% in 2025.

- The U.S. dominates the market in 2025.

Market Size & Forecast

- 2025 Market Size: USD 5.40 billion

- 2034 Projected Market Size: USD 8.95 billion

- CAGR (2026-2034): 5.8%

- Dominating Region: Europe

- Fastest-Growing Region: Asia Pacific

The market for industrial vacuum cleaner supplies engineered vacuum systems and accessories used in manufacturing plants, construction sites, food and pharmaceutical production, energy and utilities, and institutional facilities. Products range from portable HEPA-rated vacuums and canister units to large central vacuum systems, dust collectors, and vehicle-mounted units; specialised units address combustible dust, hazardous particulates, and clean-room applications.

Market Trends

Automation, Robotics, and Battery-Powered Field Equipment

The industrial vacuum cleaner market is seeing a major shift toward automation, robotics, and advanced battery technology. Facility managers are increasingly adopting autonomous sweepers and vacuum systems to reduce reliance on manual labor and improve cleaning consistency.

- For example, in June 2025, Tennant highlighted the sale of their 10,000th robotic scrubber, highlighting strong adoption in the cleaning industry and the launch of new products like the X6 ROVR.

The combination of robotics, battery power, and embedded IoT sensors is changing procurement criteria, with buyers now valuing a machine’s uptime and data services as much as its initial cost.

Emerging Markets, Rental, and Shared-Fleet Models

In rapidly industrializing regions like Southeast Asia and India, where capital budgets are limited, there is a clear trend for rental, managed-service, and shared-fleet models. “Equipment-as-a-service” allows businesses to adopt advanced vacuum technology without a large upfront capital expenditure, providing a steady revenue stream for vendors. Additionally, local manufacturing and distribution partnerships can lower costs and accelerate growth in these markets.

Market Drivers

Regulatory and Workplace-Safety Requirements

Regulations are a primary driver for the industrial vacuum market. Standards from organizations like OSHA and the EU’s ATEX directives compel companies to invest in certified equipment to protect workers from hazardous and combustible dusts. These legal and insurance pressures create a consistent demand for high-specification hardware, which in turn leads to higher average prices for compliant models. This also generates predictable, recurring revenue for vendors through the sale of consumables like filters and ongoing maintenance contracts. Companies that can provide certified and well-documented solutions gain a significant competitive advantage in regulated sectors, pushing them to invest in product certification and customer education.

Industrial Capacity Growth and Specialty Manufacturing Needs

The growth in industries that require extreme cleanliness or handle fine particulates is directly increasing demand for industrial vacuum systems. As sectors like semiconductors, pharmaceuticals, and additive manufacturing expand, they require specialized cleaning and contamination control. Facilities in these fields increasingly view industrial vacuums as essential parts of their core production infrastructure. Vendor updates from companies like Nilfisk and Kärcher show a targeted investment in these specialty industrial use cases, which confirms the strong commercial traction and long-term growth potential in these high-value sectors.

Market Restraint

Capital Intensity and Fragmented Purchasing

The high cost of advanced industrial vacuum systems, especially large central units or certified explosion-proof models, can be a major hurdle. This capital intensity often makes it difficult for small and medium-sized enterprises (SMEs) to purchase equipment outright. Additionally, the purchasing process is usually fragmented, with multiple departments involved, which can lengthen sales cycles and reduce the frequency of transactions for vendors. This dynamic forces suppliers to offer alternative options like financing, leasing, and rental or service contracts. While these models create new revenue streams, they also increase a vendor’s operational complexity and can slow down overall unit sales growth.

Market Opportunity

Service, Consumables, and IOT Subscription Models

There is a significant opportunity for vendors to build higher-margin, recurring revenue streams by bundling hardware with services and IoT subscriptions. Modern vacuums often include sensors that report data on filter life and run-time. This telemetry allows for predictive maintenance and just-in-time filter replacement programs, which facility managers value for ensuring consistent uptime and performance. Major OEMs like Nilfisk, Kärcher, and Tennant are already emphasizing service and fleet solutions.

- For instance, in June 2025, LTTS partners with Tennant to set up an Offshore Development Center, driving smart, sustainable cleaning tech and innovation across key markets.

This model reduces a vendor’s dependence on cyclical hardware sales and increases customer lifetime value, which is particularly effective in regulated industries.

Regional Analysis

Europe held a dominant share of the global industrial vacuum cleaner market in 2025, accounting for 35%, driven by its dense and mature industrial base, encompassing sectors from automotive to pharmaceuticals, which creates a constant need for specialized cleaning solutions. This is further enforced by strict EU and national regulations on workplace exposure to hazardous dusts, which mandate the use of certified, HEPA-filtered vacuums. European manufacturers, such as Nilfisk and Kärcher, are also major players, investing heavily in sustainable product lines and robust service networks. This focus on sustainability and lifecycle management, combined with a strong emphasis on automation and cleanliness in high-tech industries, makes Europe the dominant market for industrial vacuums.

The UK market is a core for industrial vacuum cleaners due to its large industrial services sector and active government support for hospitality and venue resilience. Business rates relief and other support measures help sustain a demand for commercial cleaning services. In manufacturing and construction, strong health and safety frameworks drive purchases of certified portable vacuums. Vendors are focusing on service-led models and rentals to help small businesses manage costs.

Germany is a key market because of its large industrial base in automotive, mechanical engineering, and chemicals, along with strict workplace safety and environmental rules. The country’s strong push for sustainability and circular procurement favors durable, repairable equipment and long-term service contracts. Large trade fairs and seasonal manufacturing peaks also create predictable demand for both central systems and portable vacuums. German manufacturers are well-regarded for their high-quality, robust equipment, which reinforces a healthy local supply chain.

Asia Pacific Market Trends

The Asia Pacific region is experiencing the fastest growth in the industrial vacuum cleaner market, with a CAGR of 7.9%, driven by rapid industrial expansion, significant infrastructure investment, and rising awareness of health and safety standards. Countries like China and India are rapidly scaling up manufacturing in high-tech sectors like electronics and pharmaceuticals, and new facilities are being built with modern contamination control systems. Local manufacturing also helps lower unit costs, making these vacuums more accessible to price-sensitive buyers. Additionally, rental and shared-fleet models are gaining traction, providing a way for small and medium-sized enterprises to access advanced equipment without a large capital outlay.

China’s industrial vacuum market is growing at a fast pace, fueled by massive industrial expansion and government support for modernization. Large-scale projects in electronics, automotive, and semiconductor manufacturing often include requirements for central dust extraction and validated HEPA vacuums. The combination of government policies, significant industrial investment, and a growing domestic supply network makes China a major growth market.

North America Market Trends

The U.S. market is a leader in industrial vacuum cleaners due to its strict workplace safety enforcement, diverse industrial landscape, and rapid adoption of advanced technology. OSHA regulations on hazardous materials like silica drive consistent demand for HEPA-rated vacuums and documented cleaning programs. This has led to widespread adoption in sectors like semiconductor manufacturing and pharmaceuticals.

Canada’s market is influenced by a mix of strict provincial regulations and a strong industrial sector. Occupational exposure limits and consistent enforcement encourage the use of HEPA-class vacuums in regulated sites such as mines and food processing plants. Due to its geographically dispersed facilities and high standards for environmental and worker health, there is strong demand for portable, certified units and rental services.

Product Type Insights

The portable or handheld industrial vacuum segment dominates the market and is projected to grow at a CAGR of 10.4%, driven by its versatility, mobility, and affordability, which make it a popular choice for a wide range of industries and applications. They are essential for on-site cleanup, spot cleaning, and use in confined spaces where larger, centralized systems are impractical. The continuous improvement of battery technology is also enhancing the performance of these units, allowing them to replace corded vacuums and expand their utility, making them a primary tool for facilities management, construction, and smaller manufacturing operations.

Power Source Insights

The mains or corded electric power is the leading choice for industrial vacuums, due to its reliability and the ability to provide consistent, continuous power for long-duration tasks without needing to stop for recharging or refueling. While battery technology is growing in popularity, corded models remain the standard for high-volume and stationary applications where a constant power supply is critical, such as in large manufacturing plants or centralized vacuum systems. Their proven performance and lower upfront cost also make them a practical choice for many businesses.

End Use Industry Insights

The manufacturing industry is the largest end-user segment, holding a 28% share of the market in 2025, driven by the diverse and demanding cleaning needs within this sector, which includes everything from metalworking and automotive production to semiconductors and electronics. Manufacturing processes often generate fine, hazardous, or combustible dusts that require specialized vacuum and filtration systems for worker safety and product quality. As a result, industrial vacuums are considered an essential part of the production infrastructure.

Sales Model Insights

Direct capital sales are the leading sales model, driven by the high upfront investment required for large-scale and certified industrial vacuums. This model is preferred by large corporations and regulated industries that view this equipment as a long-term asset. As the market evolves, many vendors are also leveraging this model to bundle in ongoing service, maintenance, and consumables contracts, creating a hybrid approach that secures both initial revenue from the hardware sale and a stream of high-margin recurring income.

Competitive Landscape

The industrial vacuum cleaner market is moderately fragmented and follows two primary business patterns. The first is the product-plus-service platform model, where vendors sell certified hardware, such as HEPA, ATEX-compliant, and central vacuum systems, while generating recurring revenue through consumables, validation services, and field support. The second model is rental and fleet management, in which companies provide equipment-as-a-service (EaaS), fleet telemetry, and consumables to reduce upfront capital expenditure for customers, similar to Kegstar-style solutions in other industries.

Nilfisk operates across professional and specialty segments with a mixed model, product sales for portables and central systems, plus service, spare parts, and fleet solutions that generate recurring revenues. The company emphasises sustainability and aftermarket services to stabilise margins and improve lifetime value.

Latest News

- In February 2025, Nilfisk published its 2024 results, reporting 1.2% organic growth and highlighting service- and specialty-segment improvements.

List of key players in Industrial Vacuum Cleaner Market

- Nilfisk

- Kärcher

- Tennant

- Pullman Ermator

- IPC

- Climax Portable

- Ametek

- Festool

- Bosch Professional

- Makita

- Karcher Commercial

- Ghibli (Comac)

- Hako

- Numatic

- HD (Hako/Cleanfix)

- Windsor

- Taski (Diversey)

- TSM

- Sefar

Recent Developments

- June 2025 – Tennant signed a partnership with L&T Technology Services (LTTS) to accelerate new product development, focusing on sustainable, connected industrial cleaning solutions. The collaboration aims to speed R&D for smarter, energy-efficient machines and supports Tennant’s move into IoT/telemetry and service subscription models in fast-growing markets such as India.

- February 2025 – Kärcher announced a record turnover for the 2024 financial year and reported a 4.6% increase in revenue. This momentum supports product rollouts and service expansions in Europe and APAC.

- February 2025 – Nilfisk launched three new vacuums, VP300, VP400, and VU200, as a part of its wide range of next-generation solutions to deliver greater simplicity and efficiency to users. The development of these products was driven by extensive customer research and testing.

Report Scope

Details

By Power Source,

By End User Industry,

By Sales Model,

By Region.

Europe,

APAC,

Middle East and Africa,

LATAM,

Canada,

U.K.,

Germany,

France,

Spain,

Italy,

Russia,

Nordic,

Benelux,

China,

Korea,

Japan,

India,

Australia,

Taiwan,

South East Asia,

UAE,

Turkey,

Saudi Arabia,

South Africa,

Egypt,

Nigeria,

Brazil,

Mexico,

Argentina,

Chile,

Colombia,

Explore more data points, trends and opportunities Download Free Sample Report

Industrial Vacuum Cleaner Market Segmentations

By Product Type (2022-2034)

- Portable/handheld industrial vacuums (wet and dry)

- HEPA/ULPA-filtered certified vacuums (for hazardous particulates)

- Central vacuum systems (plant/line-integrated systems)

- Vehicle-mounted and truck-mounted units

- Explosion-proof / ATEX / intrinsically safe vacuums (combustible dust)

- Dust collectors and cyclone pre-separators (industrial scale)

- Robotic/autonomous vacuum and floor-cleaning systems

By Power Source (2022-2034)

- Mains / corded electric

- Battery / lithium-ion powered

- Pneumatic (compressed air)

- Diesel / engine-driven (vehicle-mounted)

By End User Industry (2022-2034)

- Manufacturing (metalworking, automotive, electronics, semiconductor)

- Pharmaceuticals and biotech (cleanrooms)

- Food and beverage processing

- Construction and mining

- Facilities management (airports, transit, commercial real estate)

- Utilities and energy (power plants, renewables)

- Rental and service providers

By Sales Model (2022-2034)

- Direct capital sales (CAPEX)

- Rental / equipment-as-a-service (EaaS)

- Fleet management and service contracts (filters, validation)

- Consumables and spare parts programs

By Region (2022-2034)

- North America

- Europe

- APAC

- Middle East and Africa

- LATAM

Frequently Asked Questions (FAQs)

The global industrial vacuum cleaner market size was estimated at USD 5.40 billion in 2025 and is anticipated to grow from USD 5.72 billion in 2026 till USD 8.95 billion by 2034.

Regulatory and Workplace-Safety Requirements and Industrial Capacity Growth and Specialty Manufacturing Needs are some of the growth factors in the market.

The key players operating the market include Nilfisk, Kärcher, Tennant, Pullman Ermator, IPC, Climax Portable, Ametek, Festool, Bosch Professional, Makita, Karcher Commercial, Ghibli (Comac), Hako, Numatic, HD (Hako/Cleanfix), Windsor, Taski (Diversey), TSM, Sefar.

Europe dominates the global market in 2025.

The portable or handheld industrial vacuum segment dominates the market and is projected to grow at a CAGR of 10.4%.