Pat Bucher won’t be taking the Alaska cruise she had planned for her 70th birthday in October — not with her nest egg in jeopardy.

The Coram resident fears her investment adviser lost more than $200,000 she’d saved for retirement.

So Bucher is working part time and took out a home equity loan to pay her bills since the adviser stopped sending the $1,600 to $1,700 in monthly interest payments last fall.

“I trusted these people and it bit me in the butt,” she said.

WHAT NEWSDAY FOUND

- A Massapequa-based investment firm is being accused of misappropriating hundreds of thousands, and in some cases, millions of dollars of retirement savings.

- A.G. Morgan Financial Advisors LLC, CEO Vincent J. Camarda and president James E. McArthur are the subject of lawsuits, regulatory complaints and an FBI investigation, Newsday has learned.

- Camarda lost his financial planner certification and A.G. Morgan’s website is no longer operating.

Bucher is among at least 20 clients of A.G. Morgan Financial Advisors LLC who allege the Massapequa-based firm squandered their life savings, according to lawsuits, consumer complaints filed with regulators and Newsday interviews.

The losses range from hundreds of thousands to millions of dollars, affecting as many as 400 clients — many of them elderly. With their portfolios apparently wiped out, many have been forced to reenter the workforce, take on debt or lean on their children to avoid losing their homes.

In interviews, clients said they doubt they’ll ever recover their savings. A.G. Morgan appears to have shut down: Its Merrick Road office is empty, the website is offline, and the firm faces mounting legal problems, including fraud charges filed by the U.S. Securities and Exchange Commission in 2022.

The FBI has been investigating A.G. Morgan since February, according to letters to clients that Newsday reviewed. The letters say the clients may be victims “of a federal crime” and note “a large number of victims in this case.”

An FBI spokesperson in Manhattan didn’t respond to a request for comment.

The total number of investors affected remains unclear. In a filing to the SEC, A.G. Morgan reported having nearly 390 clients and $175 million in assets at the end of 2023. But in a court deposition that same year, the firm’s founder claimed 1,000 clients.

A.G. Morgan “leveraged everything and now the walls are closing in,” said Tim Dennin, a Northport-based attorney representing a retiree who fears she’s lost $450,000 because of the firm’s actions.

Dennin said subpoenaed bank records show his client’s money was shifted between accounts — like in a Ponzi scheme — but never invested.

“At the end of the day, what money is going to be available to compensate the victims?” he said.

Dennin suggested that their best hope may be a federal court-ordered restitution fund, similar to the one created for victims of Jordan Belfort — “The Wolf of Wall Street” — and his Lake Success–based firm Stratton Oakmont. Dennin represented dozens of Belfort’s victims in the 1990s.

However, with lawsuits and consumer complaints against A.G. Morgan still pending, it’s unclear if — or when — victims will see any resolution.

Northport attorney Tim Dennin, who once represented victims of “Wolf of Wall Street” Jordan Belfort, is now representing a retiree who said A.G. Morgan wiped out their life savings. Credit: Newsday/J. Conrad Williams Jr.

Neither A.G. Morgan founder and CEO Vincent J. Camarda nor president and chief compliance officer James E. McArthur responded to repeated requests for comment, including messages left with a receptionist and letters sent via certified mail to their Suffolk County homes.

When a Newsday reporter visited the firm’s Massapequa office on Aug. 6 — and on multiple occasions in June and July — no one answered the door. Online advertisements show the property is for sale.

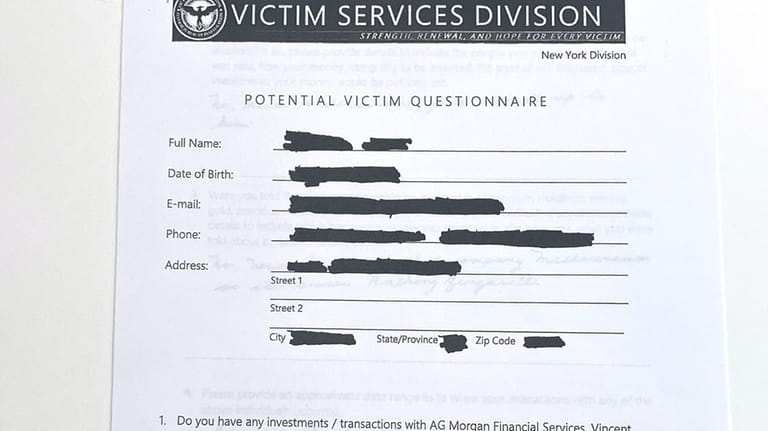

A redacted FBI “Potential Victim Questionnaire” sent to clients of A.G. Morgan Financial Advisors as part of the bureau’s investigation into the firm. Credit: Newsday

One alleged victim, a retiree in western Suffolk County, said she confronted Camarda by phone in February about the disappearance of her multimillion-dollar investment — and was met with silence. She works part time in sales and requested anonymity, saying that if customers knew about her losses, it could undermine their trust in her recommendations and jeopardize her job.

She and her late husband, himself a longtime investment adviser, had been clients of Camarda for years. They were satisfied with his performance and the investment income generated, the retiree wrote in an FBI victim questionnaire obtained by Newsday.

“I trusted Vincent as my husband did,” she wrote. “I asked very few questions as I thought Vincent was always there for me.”

As of January, her A.G. Morgan account statement — also reviewed by Newsday — showed a balance of $3.2 million and monthly interest payments of $32,545. The portfolio consisted of four funds controlled by Camarda — AGM Capital, OMNI Diversified, Wilshire Capital and Windsor Capital — each promising annual returns of between 9% and 14%.

“Since January 2024, I haven’t gotten 20 cents from A.G. Morgan and my investments,” the retiree said in an interview. Camarda “apparently lost all of it,” she said.

She said she has struggled to make sense of the loss.

“I cannot understand why this had to happen,” the retiree said, shaking her head in disgust. “It has to be greed, nothing but greed.”

Clients, regulators and the courts close in

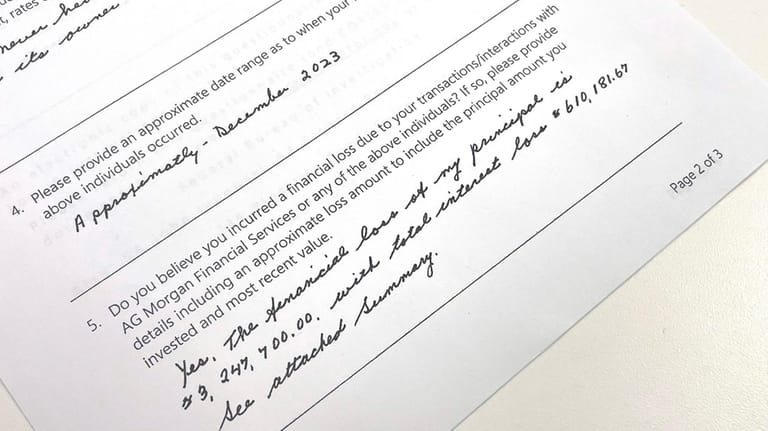

A section of an FBI victim questionnaire in which a retiree details alleged losses tied to Massapequa-based A.G. Morgan Financial Advisors. Credit: Newsday

Camarda founded A.G. Morgan in 2014 after working at several financial services firms, including more than 10 years at American Express Financial Advisors Inc. He grew up on Long Island and earned a bachelor’s degree in accounting at Hofstra University before becoming a financial adviser, regulatory filings show.

Camarda, 61, lives in Amityville and has three children. He and his wife divorced in 2011. Camarda lost most of his possessions in two house fires within two years that he said were caused by damage from Superstorm Sandy in 2012, according to his 2023 deposition to a SEC attorney and public records.

At A.G. Morgan, Camarda, who said in the deposition that he earned $60,000 per month, has in recent years steered clients away from stocks, bonds and other traditional investments and toward mining, gold, precious metals, palladium, coffee and business loans, which he promised would provide a higher rate of return.

Clients’ money was deposited in investment funds that Camarda started, managed and owned, according to the FBI victim questionnaire.

The FBI headquarters in Washington, D.C. Federal agents have been questioning alleged victims of Massapequa-based A.G. Morgan Financial Advisors. Credit: Getty Images/Kent Nishimura

Clients told Newsday — and alleged in court filings — that they received monthly interest payments for years, only to see them stop in late 2023 or last year. When the clients pressed for answers, they said they were told to be patient while one of Camarda’s business partners arranged financing to restart the payments.

The clients, frustrated by what one described as “endless lies and nonsensical excuses,” complained to the Certified Financial Planner Board of Standards Inc., which has certified more than 100,000 planners nationwide, including Camarda. His refusal to respond to board investigators led to the permanent loss of his certification in May.

Camarda is among just 63 financial planners nationwide to receive a “permanent bar” from the board since 2008, according to a Newsday analysis of enforcement actions.

“Permanent bars are rare,” said Leo G. Rydzewski, the board’s top lawyer. “CFP Board reserves permanent bars for the most egregious misconduct.”

Other A.G. Morgan clients sought recourse through the Financial Industry Regulatory Authority Inc., which oversees securities brokerages.

From 2024 through June, FINRA logged 19 complaints against Camarda, with clients seeking a total of $23.4 million in damages. McArthur, the firm’s president, faces 16 complaints, all submitted last year, seeking a combined $22.5 million in damages. None of the cases have been resolved, according to the latest available FINRA records.

Many of the FINRA complaints center on the same alleged conduct that led the SEC to sue Camarda, McArthur and A.G. Morgan in June 2022.

The SEC accused the men and the firm of recommending and selling securities without disclosing they owed $750,000 to the issuer, Philadelphia-based Par Funding. That debt created a conflict of interest and remained unpaid at the time, according to the suit filed in federal court in Central Islip.

All three have denied the allegations, and the case remains pending, according to court records. An SEC spokesman declined to comment.

The suit alleges A.G. Morgan raised more than $75 million from over 200 investors through the sale of unregistered Par securities between August 2017 and July 2020. Days after the SEC’s allegations surfaced, Par was placed in receivership. In March, Par Funding’s CEO was sentenced to 15½ months in prison for a $404 million fraud scheme.

The SEC suit states that Camarda, McArthur and A.G. Morgan earned more than $7 million from the Par Funding sales.

Camarda allegedly failed to disclose the SEC’s June 2022 action when meeting months later with prospective client Kathleen McCauley to advise her on whether she could retire from her sales job at Verizon Wireless and live comfortably into her 90s.

Inside the Massapequa office of A.G. Morgan Financial Advisors, which appears vacated. Credit: Newsday/James T. Madore

Camarda allegedly told McCauley, 68, that she “could absolutely retire today” if she invested the bulk of her retirement savings — $450,000 — in promissory notes for his Windsor Capital Fund, according to a suit that McCauley filed last year in federal court in Central Islip. The suit alleges Camarda promised a 9% return from investments in rare earth minerals, coal, limestone and kiln dust.

The Farmingdale resident began receiving $3,000 monthly interest payments in February 2023 and, feeling secure, retired that September. The payments stopped four months later without explanation, according to the suit.

McCauley, through Dennin, her attorney, declined to comment.

But in court filings, McCauley said A.G. Morgan refuses to return her money. She said she’s “tired of all the broken promises of imminent funding and litany of irrational excuses regarding the reasons for nonpayment.”

McCauley accused A.G. Morgan of engaging in “a Ponzi scheme where [her] investment returns are not contingent on any legitimate business but the receipt of additional new funds,” according to the suit.

Camarda and A.G. Morgan, in court filings, denied the allegations, saying they “acted at all times in good faith and exercised reasonable care” with McCauley’s retirement savings.

Their lawyers didn’t respond to Newsday’s requests for comment.

In Coram, retiree Bucher said the abrupt end to her monthly payments has upended her life. She needs her $205,285 investment returned immediately — but fears she may never see it again.

“I don’t have a very good feeling about how this might end,” Bucher said.

James T. Madore writes about Long Island business news including the economy, development, and the relationship between government and business. He previously served as Albany bureau chief.