Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

Today marks the one-year anniversary of my daily Substack posts. My first post a year ago pushed back on the idea that the Dollar was in freefall and the notion – popular at the time – that US reserve currency status might be in danger. I’ve learned a ton in the past year from all of you and am thankful for all the debate. I’m especially grateful to my paying subscribers who help me cover the cost of the data I use. You’re my angel investors. Thank you!

The format of what I do here is evolving. One thing I’ve started doing – in addition to my daily posts – is a weekly live stream on Saturday mornings at 9 am (ET). That’s an opportunity for live interaction and some of my more widely-read posts originate from debate on those calls. The other thing I’m starting is a Sunday post with four charts that may not fit into one of the bigger themes I’m writing about but which may still be important. Today’s post is the second in that series. I look at what may be the next big shock to labor markets, inflation and out-of-control deficits in the Euro zone.

-

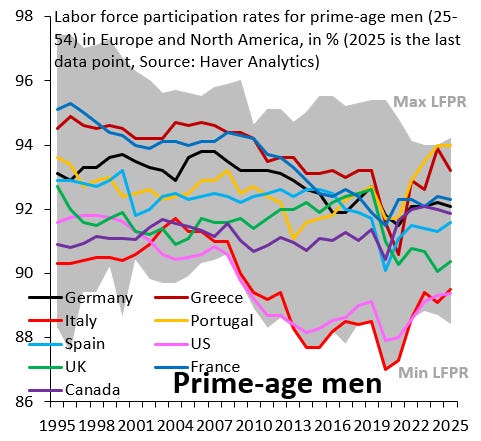

The next big shock to labor markets: there’s tons of talk about how lots of white collar jobs may be lost to AI, but I think that’s the tip of the iceberg. Think of all the work that’s repetitive and formulaic. All of that can be automated with code to a very significant degree. The only reason this hasn’t happened yet is because no CEO has ever won accolades for firing lots of people. It’s a thankless task. So the reality is that most CEOs are avoiding the issue, which means there’s a lot of hidden unemployment in our services sector. Now think about the big picture. The pink line in the chart above shows that labor force participation for prime-age men in the US is already as low as Italy (red line). Now imagine what happens when the services sector starts to automate jobs away. It feels to me like we’re on the cusp of another “rust belt” shock, only this time the rust belt will be big urban services hubs like New York, San Francisco and Washington, D.C.

-

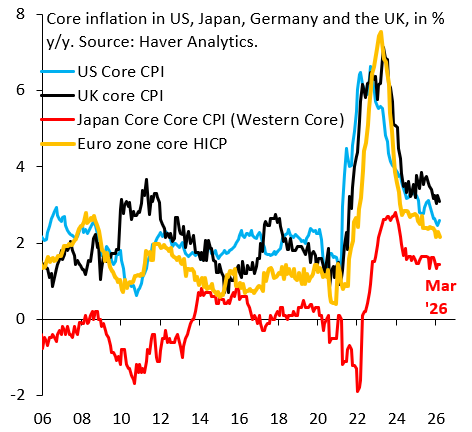

The big worry is deflation: if I’m right about the labor market, the big worry isn’t inflation, but deflation. Services sector workers will be competing for fewer jobs, which will put downward pressure on wage inflation and prices. This is why I just can’t get excited about us heading for an inflationary spiral, even though – as the chart above shows – core inflation across the world’s key advanced economies has been running somewhat “hot” since COVID.

-

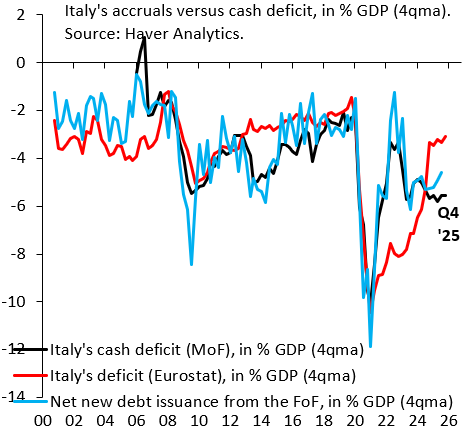

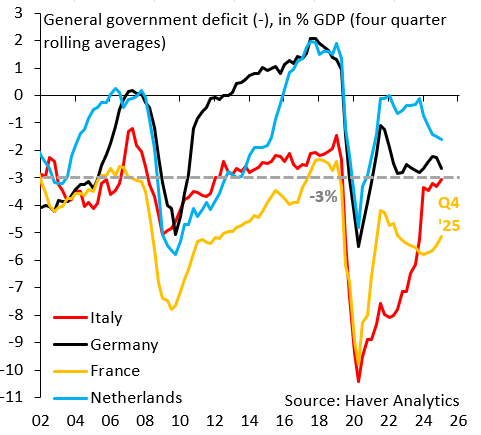

The fiscal mess in the Euro zone: the chart above shows budget deficits in what are called “frugal” countries (Germany and the Netherlands) as well as Italy and France. It’s pretty clear that fiscal policy in France is out of control and – if you’re starting to get excited about new-found frugality in Italy – please don’t. The only deficit that ever really matters is the cash deficit, because that determines the amount of debt you issue. As the black line in the chart below shows, this is far wider than the accruals deficit that’s always quoted for Italy in the press. So the truth is that fiscal policy in Italy is just as out-of-control as always. At the root of all this is the ECB, which through its past actions to cap yields perpetuates the status quo of bad policy. Politicians – like everyone else – respond to incentives. And those are broken in the Euro zone thanks to the ECB.