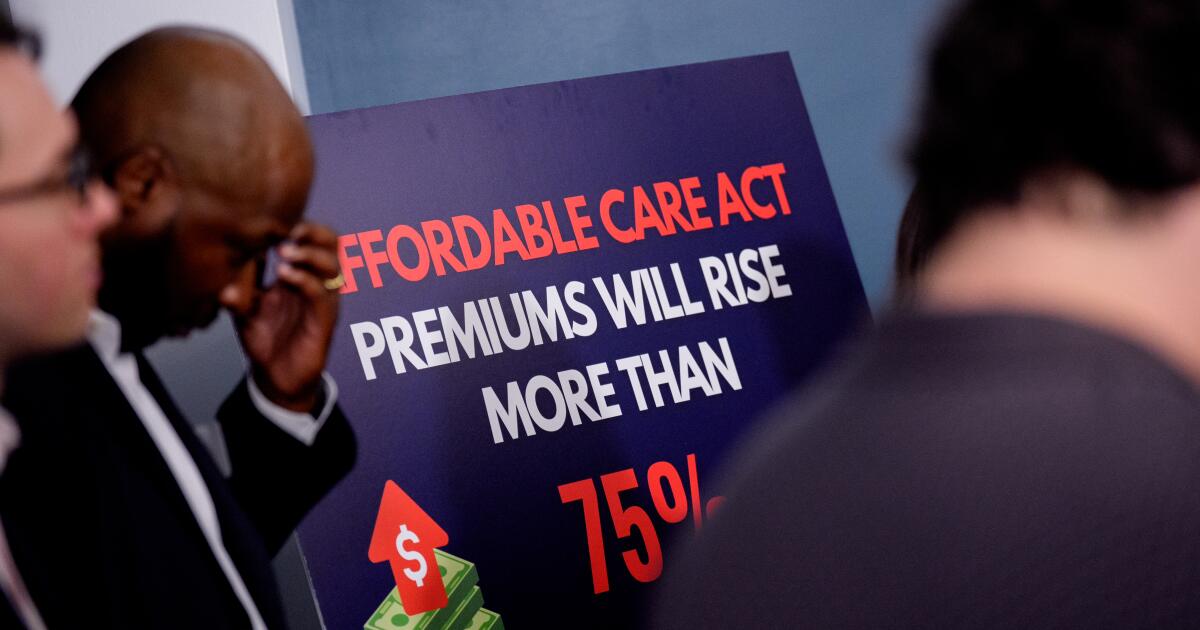

Congress ended its impasse to reopen the government, but the Democrats’ reason for the shutdown remains unresolved: the renewal of expiring subsidies for insurance premiums under the Affordable Care Act.

Republicans offered an olive branch to end the standoff by proposing to make payments into Americans’ health savings accounts or flexible spending accounts. Although this idea was not realized, the proposal should not be forgotten as the parties work on compromises for long-term government appropriations. The Republicans’ plan would allow individuals to choose between putting the money toward insurance premiums or spending it directly on healthcare. This offers a refreshing change from the top-down approach to healthcare that has dominated both political parties for generations.

Moving away from insurance subsidies and directing payments to taxpayers would serve as a first step toward empowering Americans to make their own healthcare choices and leverage their self-interest to contain healthcare costs. Americans would be incentivized to curb spending and would have the upper hand in bargaining for lower costs with providers. This approach offers a path for opening up access to healthcare while addressing the underlying problem plaguing our system: healthcare inflation.

When politicians talk about containing the escalating healthcare costs, they take a top-down approach that fails fundamentally to change the face of American health care. Just as the Biden administration negotiated for price caps on prescription drugs used by Medicare recipients, President Trump recently negotiated a price drop for anti-obesity drugs. These gimmicks grabbed headlines but did little to address a persistent paradox: while healthcare costs vastly eclipse inflation, healthcare innovation has flattened.

The Affordable Care Act, Medicare and Medicaid suffer from similar flaws as top-down health reform initiatives that expand access at the cost of our system’s long-term viability. Their reimbursements have focused on short-term cost-cutting that ends up stifling competition, crippling innovation, and raising long-term costs. The Affordable Care Act’s cost-cutting centerpiece is higher government reimbursements for “coordinated care,” with the well-intended logic that economies of scale through integrated networks are the best way to expand access and cut short-term costs. This approach has “worked” inasmuch as reimbursement incentives have led small physician practices to merge en masse and prompted private equity to buy out freestanding medical centers. The result is regional oligopolies and closures of rural hospitals. For every dollar saved through consolidation, more is being spent on the endlessly growing compliance red-tape that buries doctors in paperwork and distracts them from patient care.

We don’t have to settle for a managed decline of our healthcare system. Both parties have said they want to make the Affordable Care Act “better.” The Republicans’ proposal of contributions to health savings accounts or flexible spending accounts would represent a first concrete step.

Hospitals often charge several times more for procedures when insurance or government reimbursement is used than when paid in cash. Those with annual HSA or FSA grants could pay the lower prices and contain healthcare costs. Instead of letting insurers dictate which procedures patients can and cannot access, the government would let patients take ownership over their healthcare.

The government can also motivate people to be good stewards by allowing them to retain unspent medical funds for future health expenses. By working through consumer advocacy groups to negotiate cash prices and by taking advantage of policies on pricing transparency, patients would have a personal stake in their health and be more informed consumers. Empowering consumers may also incentivize the marketplace to innovate based on consumer demand and help hospital systems better discern which services are valued.

The past two generations of healthcare have been about gradual socialization of medicine, which has subordinated both patients and doctors to faceless bureaucrats and insurers. But the recent Republican proposal to direct supplemental payments to HSAs and FSAs, coupled with transparency requirements for healthcare costs, offer a way to put patients back in the driver’s seat. Our leaders would do well by empowering consumers to make healthcare choices and by embracing a bottom-up approach to cost management and innovation. This is the best pathway to making care both accessible and affordable.

Kim-Lien Nguyen is an associate professor of medicine at David Geffen School of Medicine at UCLA and a practicing cardiologist.

Insights

L.A. Times Insights delivers AI-generated analysis on Voices content to offer all points of view. Insights does not appear on any news articles.

Perspectives

The following AI-generated content is powered by Perplexity. The Los Angeles Times editorial staff does not create or edit the content.

Ideas expressed in the piece

-

The current approach of subsidizing insurance premiums through the Affordable Care Act represents a top-down healthcare system that fails to address underlying cost drivers and stifles innovation in the marketplace. Instead of renewing expiring ACA subsidies, Congress should redirect those payments to Health Savings Accounts and Flexible Spending Accounts, allowing individuals to choose whether to apply funds toward insurance premiums or spend them directly on healthcare services.

-

Empowering consumers to make their own healthcare choices creates personal financial incentives to curb unnecessary spending and negotiate directly with providers for lower costs. When patients have control over healthcare dollars and awareness of prices, they can take advantage of price transparency requirements to identify more affordable options, much like cash-pay patients who often access procedures at significantly lower rates than insured patients.

-

The consolidation of hospitals and physician practices resulting from ACA reimbursement incentives for coordinated care has created regional oligopolies and contributed to rural hospital closures, representing a managed decline of the healthcare system rather than genuine innovation or improved access. This demonstrates how government policies intended to contain costs through top-down coordination ultimately raise long-term expenses and limit consumer choice.

-

A consumer-driven model where individuals retain unspent medical funds for future expenses and work through consumer advocacy groups to negotiate prices represents a fundamentally superior approach to healthcare reform compared to decades of gradual socialization of medicine that has subordinated both patients and doctors to faceless bureaucracies and insurers.

Different views on the topic

-

Enhanced ACA premium tax credits currently assist more than 22 million people in obtaining affordable coverage, with these credits saving subsidized enrollees an average of $705 annually and reducing annual premium payments to $888[5]. The enhanced subsidies have proven transformative for access, spurring a 50 percent reduction in the uninsured rate among adults ages 50 to 64[5] and growing overall Marketplace enrollment from 12 million in 2021 to a record 24.2 million in 2025[5].

-

If enhanced premium tax credits expire at the end of 2025 as currently scheduled, premium payments for subsidized enrollees would more than double, increasing by an estimated 114 percent from an average of $888 in 2025 to $1,904 in 2026, representing a loss of approximately $1,016 annually per enrollee[2]. Additionally, the Congressional Budget Office projects that expiration of enhanced subsidies would result in a decline of more than 2 million people enrolled in ACA exchanges, as those dropping coverage would likely have lower healthcare costs while remaining enrollees face higher premiums due to adverse risk pool changes[1].

-

The subsidy cliff returning in 2026 would eliminate all subsidies for individuals with household income exceeding 400 percent of the federal poverty level, effectively removing financial assistance for middle-income enrollees and older adults not yet eligible for Medicare who depend on Marketplace coverage[5]. This represents a significant barrier to coverage access and affordability for vulnerable populations who currently benefit from the removal of income caps under enhanced subsidies[4].

-

While HSAs and FSAs offer tax advantages for those who can access them, these accounts have limitations that differ fundamentally from premium subsidies—FSAs are subject to “use it or lose it” rules with annual limits of $3,300[3], and HSAs require enrollment in high-deductible health plans that may not be accessible or affordable for lower-income individuals who currently benefit most from direct premium assistance[1][2].